📰 The MSM wrap-up

Does the MSM control the property market narrative?

What’s on our mind: Does the mainstream media (MSM) impact buyer/seller sentiment? We think so… but how much of the news should we trust?

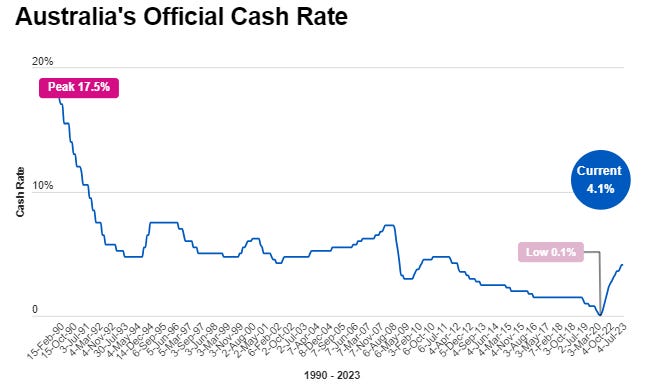

What happened this week: RBA kept rates on hold at 4.1%

What are we watching next week: New Zealand cash rate decision, RBA Governor Phillip Lowe’s speech (Wed 1:10 pm), US inflation rate and Canada’s cash rate decision.

Prelude:

What’s on our mind:

Where does someone look to see what is happening in the Australian property market?

Mainstream media outlets like Realestate.com.au (REA) and The Australian Financial Review (AFR).

For context:

Realestate.com.au has >12 million Australians visiting its website every month.

AND

The Australian Financial Review has an average monthly audience of ~4 million Australians.

With large user bases, media outlets can influence how people think and ACT.

By putting out positive articles, suggesting property prices are about to rocket higher, the media outlets could influence a homebuyer to bid an extra $10,000 at an auction on the weekend.

By doing the opposite, the media outlets can scare buyers and lead to lower demand.

This week we look at what the mainstream media is saying about the Aus property market.

Must read mainstream media articles:

(Source)

The TLDR:

Insolvencies in the building sector are up 75% compared to last year.

Margins are shrinking industry-wide.

Labour shortages are leading to increased costs.

High-interest rates and rising prices are putting new projects on hold.

Our take on labour costs:

Construction costs are increasing NOT because of materials shortages but due to labour shortages.

In markets, there is an old saying that “the cure for high prices is high prices”.

The thinking is that if prices stay high enough, it leads to decreased demand and then eventually lower prices.

We think that eventually, labour costs will start to come down as tradies are forced to compete on winning a smaller pool of work.

Our take on builders:

As for the builders, in the article, Professional Builders co-founder Russ Stephens says builders that don't carry significant reserves (cash balances) would be found out.

The reality is that the builders rarely carry significant cash reserves.

The only thing keeping builders solvent is the NEW work they are winning.

Without NEW work, the builder has no way to pay off the losses from projects taken on during the pandemic and no way of paying for overheads (which have increased due to workloads increasing).

We expect new work to dry up significantly over the next nine months, leading to even more insolvencies.

Here are some signs we look for when assessing whether or not a builder is in a strong financial position:

Job sites are inactive for extended periods - this likely means they aren't paying trades OR are having trouble getting trades onto a site which is never what you want to see from your builder.

Your builder is hard to reach - it's never a good sign if the builder isn't answering or, worse yet, dodging your calls.

Aggressive marketing - most builders we speak to are flat out at the moment. If a builder has been in the industry for decades but is offering massive discounts, this is something to be cautious about.

Heaps of jobs started in 2020-2021 that still need to be finished - this needs no explaining... Builders are in the turnover game; if they aren't finishing jobs, they aren't making any money.

(Source)

The TLDR:

Distressed sales are up 11.1% in NSW and 19.7% in Victoria.

Mortgage holders with $600k debt now paying $15,000 more than in May 2022.

“increased the risk of a “double-dip” downturn.”

Our take:

Increased distressed sales are no surprise to us.

Interest rates have gone from 0.1% to now sitting at 4.1%, the fastest increase in the history of Australia.

While we think there is still another rate hike or two left in the RBA, the real kick in the stomach to the property market will come from the fixed-rate mortgage cliff that we have written about in the past.

See our article on the mortgage cliff here: The coming fixed rate mortgage cliff.

We expect the pain to start in the September quarter this year and run through to the end of the March quarter of 2024.

We think the bottom in the property market won't be until we have seen lower prices and an RBA that’s starting to talk about rate cuts.

Our view is that rate cuts come AFTER the property market bottoms.

(Source)

The TLDR:

Prices reached a peak across ~15% of suburbs across the country.

% of suburbs hitting new highs - Perth 58.7%, Adelaide 39.9%, Darwin 11.6%.

Our take:

If you are a property investor/owner, the headline makes for a dopamine hit.

But toward the end of the article, after reading about massive gains in Perth, Adelaide and Darwin, it is obvious prices aren't rising across the country.

The highs are focused explicitly on NON-east coast states.

Of course, the east coast is where most of the bubble was inflated during the last three years.

The article later admits that only 1.6% of suburbs hit new highs in Melbourne, and only 0.8% hit new highs in Sydney.

Ultimately headlines like this are just “noise”. The property bubble in Australia is concentrated in Sydney and Melbourne, and we think most of the pain will be felt across those two cities.

(Source)

The TLDR:

Aus cash rate is 4.1%, compared to the US at 5%, Canada at 4.5%, and NZ at 5.5%.

Labour costs increase, leading to wage/price spiral and services inflation.

Unemployment is still near record lows of 3.6%.

Central bank rate hikes haven't had an impact YET.

Loan defaults are increasing at the highest levels since 2010.

Our take:

While the article is more focused on financial markets, Chris Joye sets the scene for the outlook on interest rates.

We agree with Chris that inflation is a lot stickier than anyone could have expected and that cash rates are likely to go higher from here.

We also agree that the rate hikes have barely impacted consumer demand preferences.

Chris’ article gets a bit technical toward the end, but it's still a good read if anyone wants to get an idea of where they think rates are headed in the short-medium term.

The key takeaway for us is that the impacts of the rate rises by the RBA are yet to be felt in the property market.

(Source)

The TLDR:

CoreLogic says, “Higher interest rates and lower sentiment to weigh on demand”.

High prices in early 2023 result from low supply, increased immigration and softer messaging on rate hikes by the RBA.

Rents increased by a further 0.7% in June.

Our take:

A relatively balanced article.

Highlights what's propping up the market and what we think will lead to its demise.

A lot of the buying early in 2023 has come from those thinking RBA rate hikes are over or are close to a peak.

For some reason, buyers think that is good news...

We wrote about why we think it isn't in last week's article: Rate Hikes paused

Our view is that more supply will eventually more supply will come online.

Over-leveraged investors, developers and homeowners who see prices “rising” will look to take advantage of the more buoyant market and list their properties.

We expect more supply to come online at the same time as the cohort of prospective buyers decreases.

Eventually, just like any supply/demand curve, supply will exceed demand, and prices will decrease until more buyers come back into the market.

We have also written about the property/supply-demand outlook in a previous article which can be read here: Australian Property Supply and Demand.

Thanks for reading,

Aus_Prop team.

You can contact us here:

On Twitter @Aus__Property

Via email at Auspropertymarket@gmail.com

Or through Substack - Property Down Under

Loved this !!!!