Australian Property Supply and Demand

our 2023 outlook...

Will we see housing supply outstrip demand in 2023?

What’s on our mind: Our thoughts on supply and demand in the property markets over the next 6-12 months.

What happened this week: The US Federal Reserve increased rates to between 4.5 to 4.75%. Lending for housing is down ~30.5% from its Jan-2022 peak.

What we are watching next week: Reserve Bank Of Australia cash rate decision on the 7th of February 2023, 2.30 pm (AEDT).

Prelude:

What’s on our mind:

The US Federal Reserve increased its policy interest rate by another 0.25%.

The increase takes the US Fed funds rate to between 4.5 per cent and 4.75 per cent - the highest level since September 2007.

Immediately after the decision Powell held a press conference where he discussed the path forward for interest rates, softening inflation data and how close the Fed was to bringing inflation back in check.

The entire press conference here

At the highest level, the conference was about letting markets know that the war against inflation was not over.

Powell was careful to send the markets a message that more rate hikes are on the horizon and that cuts were not even up for consideration yet.

This sounds good and well, but the underlying message from the world's most influential central bank was that we are approaching a peak in interest rates.

While we expected the rate hike, it's what Fed chair Jerome Powell said in his press conference that surprised us.

It was Powell’s focus on inflation in the ‘services sector EXCLUDING housing’ that had us interested.

Powell made it very clear in his press conference that the US Fed was more focused on “non-housing services” - a category that makes up more than 50% of the inflation index.

Powell clearly said that the Fed is simply not focused on the housing sector as much as it is on the services sector.

After all, the US already went through a housing & banking crisis back in 2008-2009.

The resulting global financial crisis (GFC) forced the US banks into a period of restructuring.

So why is this comment so important, and how does it relate to Australia?

Simply put, the Reserve Bank of Australia is fighting the same inflation battle, BUT we can't afford to ignore what the housing sector is telling us.

Construction is one of the biggest contributors to Australia’s Gross Domestic Product (GDP) and the residential property market is collectively valued at $8.1 trillion - 4x the size of Australia’s economy (GDP).

As a result, we suspect the Reserve Bank Of Australia is placing a lot more emphasis on potential issues in the housing sector relative to the US Fed.

This would also explain why Australian cash rates are much lower than its G20 counterparts like the US & Canada.

One of the indicators we think the RBA is watching like a hawk is credit growth which we think is a leading indicator for DEMAND in the property market.

To illustrate this point, we looked at the latest lending data released by the Australian Bureau of Statistics (ABS) for the month of Dec-2022.

The data showed an overall decline in lending for housing of 4.3%.

As of the end of December, total lending for housing was down ~30.5% from its Jan-2022 peak.

Source: Lending indicators

What looked like a ‘minor retracement’ a few months back is now firmly in the ‘significant correction’ category.

The connection to DEMAND?

Most property purchases are funded by high LVR (Loan to Value ratio) mortgages.

Declining lending in the housing sector ultimate impacts DEMAND.

Simply put:

Lending ⬇️ = ⬇️ in $ value demand for property.

No matter how strong the Australian appetite to buy property is, reduced lending has this impact.

But what about SUPPLY?

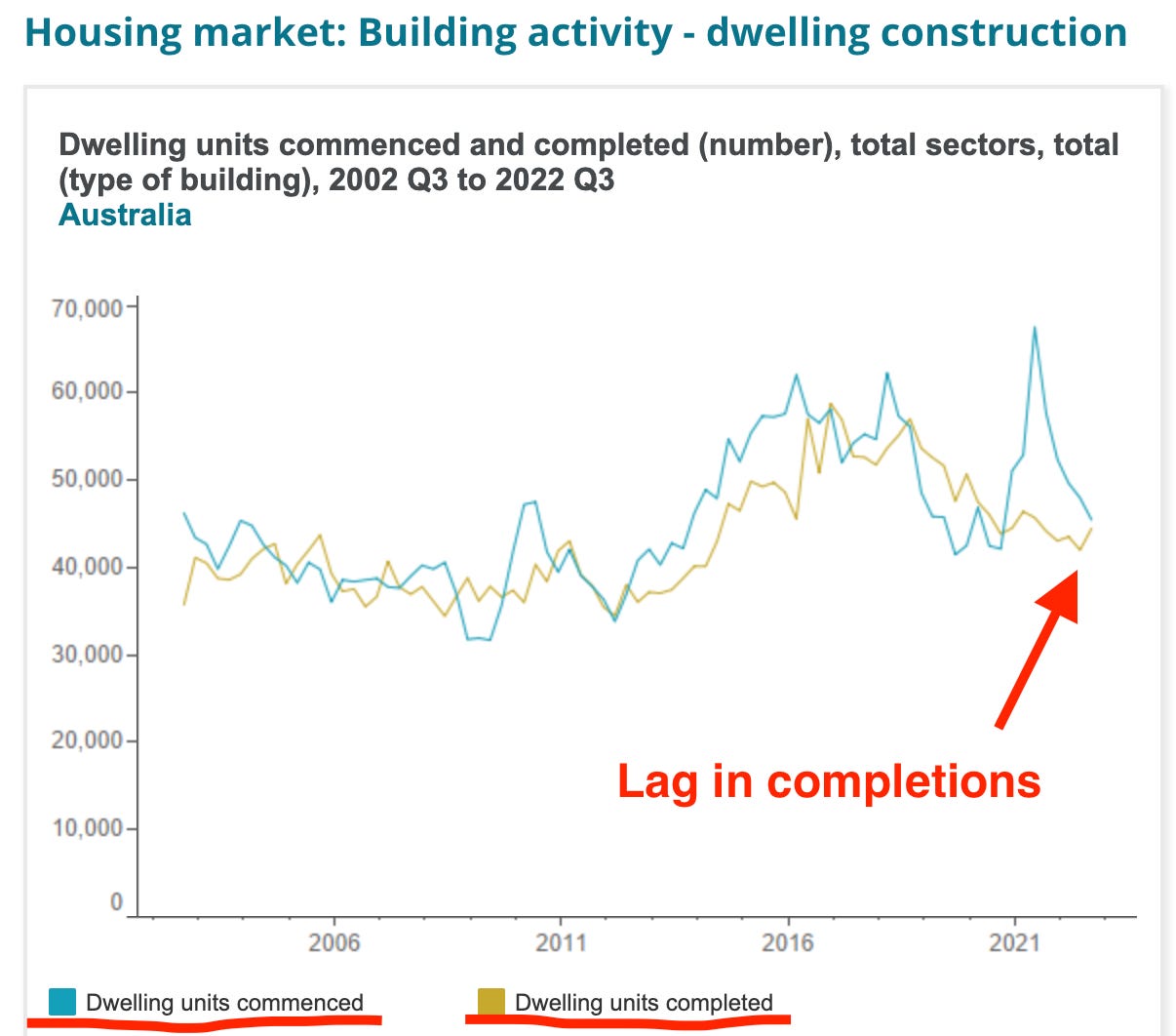

We looked at the following data released by the Australian Bureau of Statistics (ABS) on dwelling commencements and completions.

Source: Housing market: Building activity - dwelling construction

The image shows that while the building and construction industry saw a record in commencements, COMPLETIONS didn't follow through.

Completions ultimate mean more supply.

Under normal circumstances, we expect the lines to follow after one another, with completions lagging commencements by <12 months.

This time COVID’s impact on supply chains meant builders couldn't find the materials needed for projects to finish.

Then in 2022, rate hikes made funding harder to find, compounding the delays.

On the supply side, we have COVID and rate hikes impacting how quickly builders/developers can bring supply to the market.

Anecdotally (and of course, this isn't something anyone should rely on), we are noticing builders are as busy as they have ever been, AND developers are just getting around to finishing the projects that were approved in the boom years.

Source: Housing market: Building activity - dwelling construction.

What does this tell us?

With materials shortages less of an issue now and labour relatively easier to find, our view is that completions should start to increase in 2023 and 2024.

We expect to see a lot of the supply that couldn’t come to market in 2021-2022 finally hit the market this year.

More dwelling completions will = MORE SUPPLY.

Bringing everything together:

LOWER DEMAND = Slowing lending in the housing sector as a result of higher interest rates will mean lower $ value demand for housing.

HIGHER SUPPLY = Materials shortages are a thing of the past, a lot of the supply that was meant to come to market in 2021-22 will come to market this year and into early 2024.

Demand ⬇️ + Supply ⬆️ = Prices ⬇️

While the long-run supply/demand equation may look a lot different, we think the next 1-2 years will see reduced demand and an excess supply contributing to reduced property prices.

This may present buying opportunities for those who are prepared, but more on this in another email.

Contact us at Auspropertymarket@gmail.com and tell us what you think will happen to property prices this year.

Thanks for reading,

Aus_Prop team.

On Twitter @Aus__Property

Via email at Auspropertymarket@gmail.com

Or through Substack - Property Down Under