Rate hikes paused

Here we go again…

When the rate rises stop, the clock starts ticking.

What’s on our mind: Rate hikes on pause, rate cuts next? - Why all of this is terrible news…

What happened? Reserve Bank of Australia keeps rates on hold at 4.1%.

What are we watching: US unemployment rate numbers later this week

Prelude:

What’s on our mind:

The RBA just kept rates on hold at 4.1% - BUT is this good or bad news?

Straight off the bat… we think it means bad news.

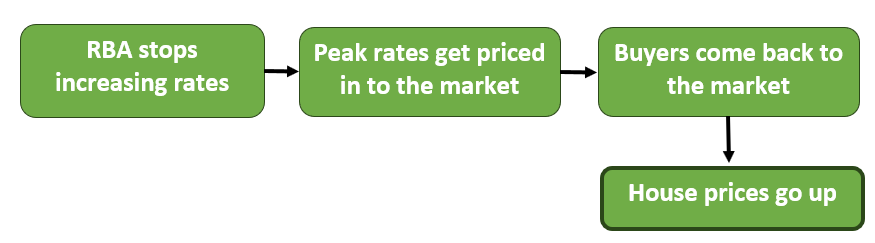

The mainstream point of view is that rates are getting close to a “peak”.

The thinking is that when rate rises are paused, the market will turn, and positive sentiment will return.

The theory is:

The “experts” want us to believe that when the RBA has stopped hiking rates, it acts as a metaphorical gunshot to a sprint race of buying in the property sector.

Theoretically, it sounds like the market could play out that way…

After all, if rates are not rising, are they not more likely to be cut?

The reality is that a pause in rate hikes usually smells like trouble for the property market.

The “experts” seem to gloss over the fact that any pause is usually a response by a central bank to signs of distress.

If a central bank thinks it's time to pause rate hikes, they see turmoil in credit markets or a slowdown in the domestic economy.

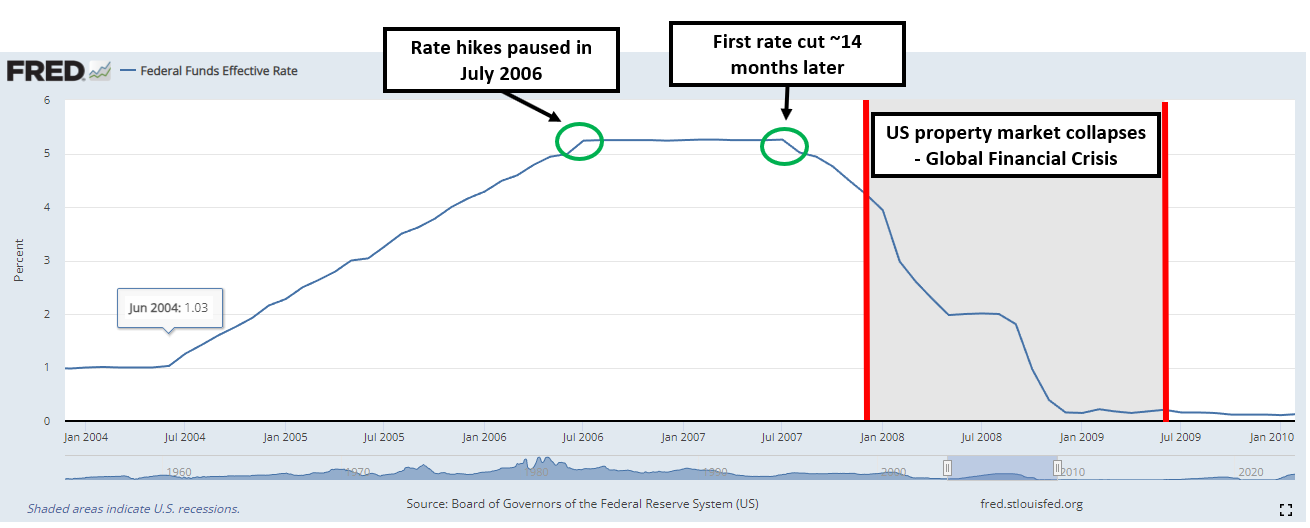

Today we look at the U.S. housing bubble of the late 2000s and see what happened after the U.S. Fed stopped raising rates in 2006.

The U.S. housing bubble - what happened after rates stopped rising?

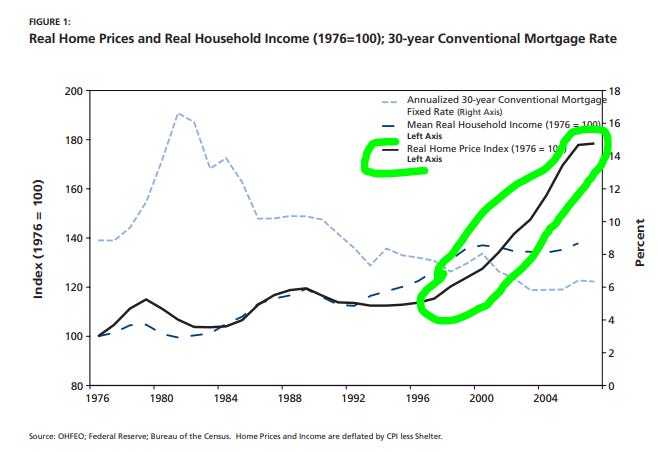

Let's go back to ~2004 when the property market had just started heating up.

In the early 2000s following the tech crash, the U.S. Fed cut interest rates to ~1%.

Over the next 6-7 years, property prices started rising significantly.

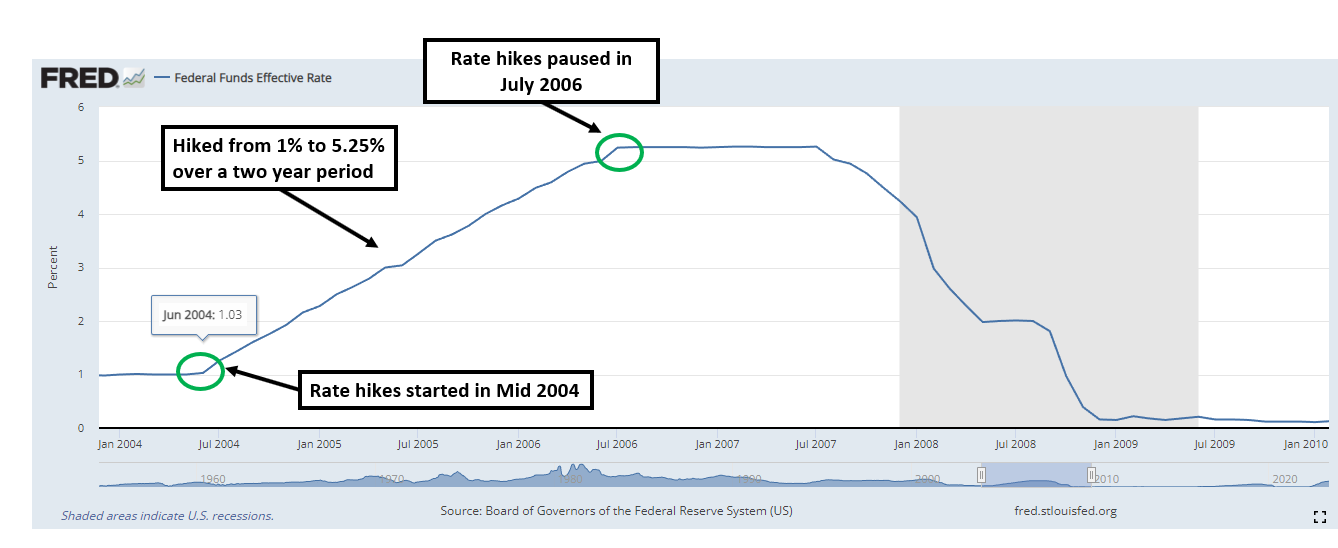

Responding to a heating up housing sector and inflation rates in mid-2004, the U.S. Fed started increasing rates.

Rates kept going up until mid-2006 and peaked at ~5.25%.

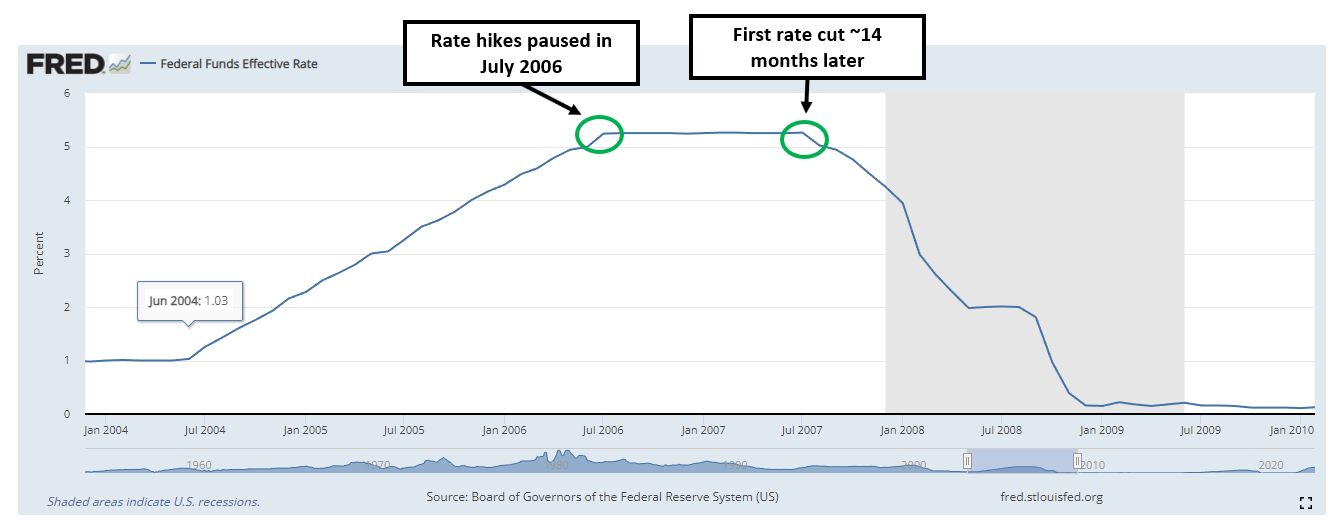

Rates eventually stopped rising in July 2006.

Rates had stopped rising, but cracks started appearing in the U.S. economy.

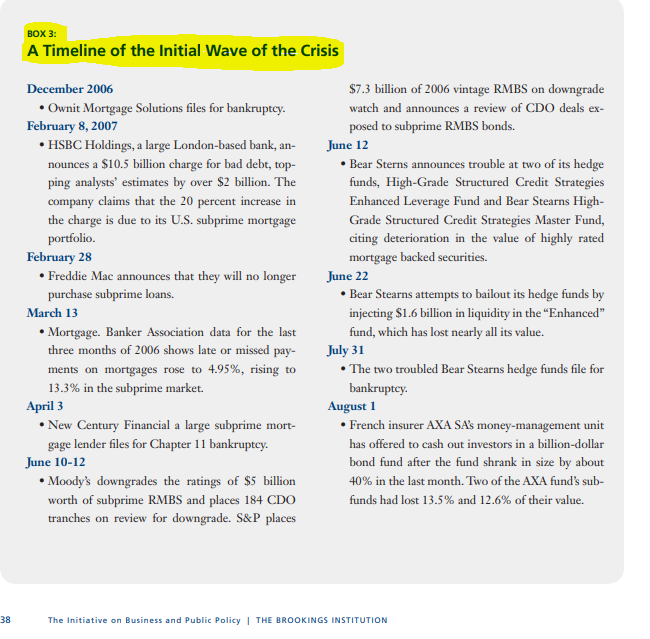

In December 2006 ‘Ownit Mortgage Solutions’ filed for bankruptcy.

April 3rd 2007 - ‘New Century Financial’, a large subprime mortgage lender, filed for bankruptcy.

By July 2007, two troubled Bear Stearns hedge funds with exposure to property debt filed for bankruptcy.

In August, the problem started spreading to the rest of the world, and German bank IKB Deutsche had to be bailed out by a German state-run bank due to troubles from exposure to U.S. Subprime loans.

On August 6th 2007 ‘American Home Mortgage Investment Corp’ filed for bankruptcy.

Eventually, ~1.5 years after the pause in rate hikes, the market implosion was getting out of control, and the U.S. Fed started cutting rates.

On August 16th 2007, the Fed cut rates for the first time in ~14 months.

But what followed wasn't a period of calm OR a roaring recovery in property prices.

In fact, the situation got a whole lot worse.

By March 2008, banks in the U.S. and worldwide had suffered billions of dollars in write-downs, and Bear Sterns was sold off to JP Morgan for US$2 per share.

The bank's share price was ~US$165 a year ago.

Things got even worse in September 2008 when Lehman Brothers, one of the USA’s biggest banks (at the time), went bust.

We could go on about the Global Financial Crisis for days, but the key takeaways for us are:

The U.S. Fed pause in rate hikes signalled the top of the market.

For the 12 months after the pause, cracks in the economy started appearing.

Only ~14 months later, the FED began to cut rates as companies exposed to the property sector filed for bankruptcy.

The U.S. Fed rate cuts coincided with the collapse in the property sector.

So while market commentators want us to believe that rate pauses and hikes are GOOD for the market - history tells us it is nothing but bad news…

For those interested, the following publication gives an excellent month-by-month summary of the lead-up to the GFC in 2008.

(Source)

Why doesn't the market recover when rates stop rising?

From this point onwards, it is all OUR opinion, but we think the reasons are as follows:

Pause in rate hikes and subsequent rate cuts mean the system is failing.

A pause in rate hikes generally is a response by the central bank to a slowing economy.

Rate cuts are merely an extension to that response and usually a sure sign that things have started breaking.

At a high level, we see both of those moves as an admission by central bankers that the economy is moving into a period of distress… not into a period of prosperity.

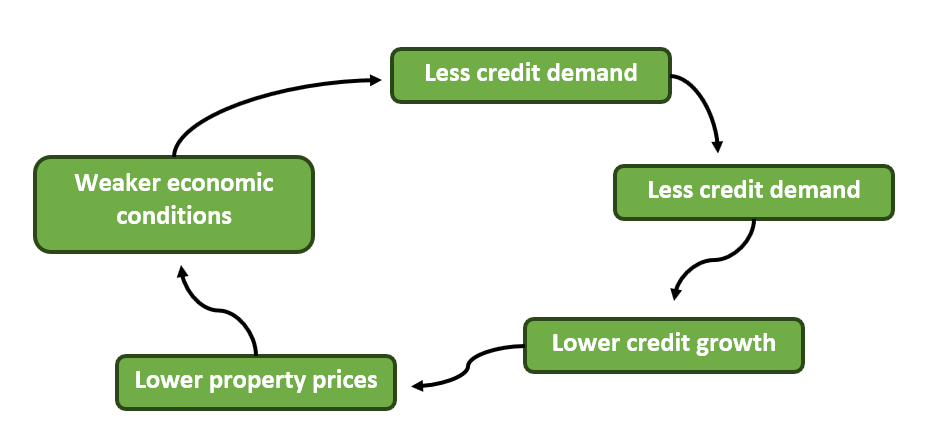

When the economy starts to slow, banks stop lending (or at least want to stop lending).

AND without new credit growth, property prices start falling.

The whole thing sets off a negative feedback loop of:

The cycle repeats until the central bank cuts rates back to a level where demand for credit starts to normalise, and we start to see a pick up in new credit.

That process can take years/decades to sort itself out.

How we are monitoring the market:

We are ignoring the noise:

Low supply means prices will stay high -

We think prices remain high UNTIL supply comes onto the market, which we believe it will…

See our previous note on this here.

Immigration will mean more demand for property and higher prices -

Immigration was net negative across the eastern states during the 2020-2021 increases in property prices.

We think immigration has less impact on prices than credit growth.

We believe immigration impacts rental demand more than it does existing dwellings.

Rate rises will stop - for all the reasons discussed today. This is not good news…

We are watching credit growth data on a monthly basis.

If we continue to see credit growth fall, prices will eventually follow.

Subscribe to stay up to date with our updates.

Thanks for reading,

Aus_Prop team.

You can contact us here:

On Twitter @Aus__Property

Via email at Auspropertymarket@gmail.com

Or through Substack - Property Down Under

Not that I'm optimistic but the other thing to note is the quality of the loans were poor, apparently loans were given to anyone and everyone.

Nothing applies to Aus Prop sector . Here in lucky country the Politicians own multiple inv prop and its too big to fail. they will keep running ponzi economics and import more migrants ( on dole if necessary) to keep housing shortage a long term goal