Rates rising - will more housing stock arrive?

Rates rising - will more housing stock arrive?

Prices to fall?

Spring stock on its way, rates rising, house prices to fall?

What’s on our mind: This week, we think about the next six months, more housing stock, higher rates and a market in turmoil?

What happened this week: European central bank raised interest rates by 0.5%. RBA governor Phillip Lowe said:

“The time of really low-interest rates is over.”

“The neutral nominal rate must be at least 2.5%. If medium-term inflation expectations were to rise, it would be greater than this”.

What are we watching next week: US Federal Reserve rates decision, Australian consumer price index data, Business confidence data, retail sales data.

Prelude:

The property market winter is coming.

More listings in spring + higher interest rates = Lower prices?

What’s on our mind:

The question plaguing our minds this week was the following:

How much more housing stock is listed for sale in spring versus the winter months?

After all, prices are a function of supply and demand.

The next step is pressure on prices if we have more houses listed for sale than buyers in the market.

The thinking behind this being buyers have a bigger range of opportunities to pick and choose from, forcing vendors to compete against one another on pricing.

Going into the back end of this year, we think the following is occurring:

Supply INCREASING - Vendors are forced to put properties up for sale when interest rates rise and servicing debt becomes more expensive, along with vendors returning to sell after the winter months have passed.

Demand DECREASING - With interest rates rising and the RBA governor saying “X”, taking out a loan and servicing it is becoming more difficult, forcing potential purchasers to delay buying decisions.

This week, internally, we debated the supply/demand outlook for the property markets over the next six months.

First - Supply

After going on a bit of a fact-finding mission found the following data trying to answer the question:

Historically, how much more stock is there in spring vs winter?

During the Sydney winter months last year, there was a total of ~74,586 listings, compared with 82,544 in spring.

So the answer to our question was 11% more.

This very quickly gives us an answer to how supply may be impacted.

A hypothetical - if there are 100,000 homes for sale right now, we should expect to see 111,000 homes listed in spring.

Add to this potential selling from those who find themselves over-indebted and struggling with the increasing RBA cash rate, and we think we will be entering a period where we have a lot more stock available for buyers.

(We will discuss why we think no one is talking about those over-indebted sellers later in today’s article).

Second - Demand

As mentioned earlier, this isn't just a supply story, though. Demand also matters.

This is where AGAIN, rising interest rates come into play.

We will keep this part of the article short and sharp by quoting old mate Phillip Lowe (governor of the RBA and the gatekeeper of the Australian economy), who said in a speech this week:

“The neutral nominal rate must be at least 2.5%. If medium-term inflation expectations were to rise, it would be greater than this”

It's almost as if he woke up one morning, looked at market expectations for the cash rate and realised he might be behind the curve.

“Behind the curve” basically means the RBA need to increase the cash rate to catch up to where the market thinks the cash rate should be.

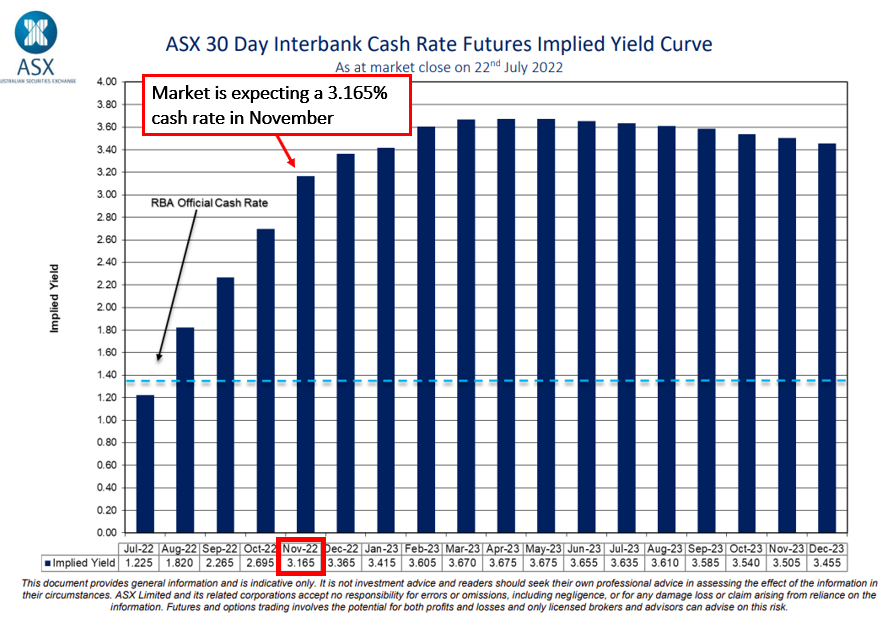

So where does the market see the cash rate in, let's say, October?

So the RBA governor and the market are signalling a cash rate of 3%+ by the end of the year. What does this mean for mortgage rates?

If we use our formula for calculating mortgage rates, we get the following:

(1) Funding costs 3.165% + (2) Net interest margin 2.25% = (3) Mortgage rate offered to new borrowers 5.415%.

(To see how we got to this formula, read our previous article: How do mortgage rates rise?)

Mortgage rates of 5.4% or higher would be 3x HIGHER than the fixed rate loans offered to new borrowers in mid-2021, as low as ~1.8%.

As the cost to borrow increases, people take out smaller loans or, even worse.. defer purchasing until they can afford to service a loan again.

This DECREASES demand.

With that, we have an answer to the demand side of our equation.

SO let us summarise the above:

Housing stock in spring UP - 11% more stock coming to market = SUPPLY ⬆️

Cash rate UP - Expected to go above 3% = DEMAND ⬇️

We think the market is entering a 3-6 month period where supply is increasing and demand is decreasing.

The direction for property prices with this backdrop can only be in one direction….⬇️

Why do we think this spring will see more housing supply than usual?

The answer to this question is relatively simple.

Increasing interest rates = rising debt servicing costs.

Increasing debt servicing costs = puts pressure on household budgets

Household budget pressures = households look to sell assets and pay down debt.

But to understand how this works, we need to understand what debt is and the difference between GOOD and BAD debt.

First, what is debt?

Debt is simply buying power. A bank provides you with a loan, and in exchange, you have the financial ability to go and make the purchases you want.

There can be such a thing as “Good debt” and “Bad debt”, easily classified as follows:

Good debt = Borrowed money used productively, generating sufficient income to service the debt.

Bad debt = Borrowed money that is used unproductively. Either in properties that are negatively geared or don't bring in any cashflows.

Famous investor Ray Dalio, who we mentioned in last week's article (Australian property in a bubble?), puts it this way:

“Debt that produces enough economic benefit to pay for itself is a good thing. But sometimes the trade-offs are harder to see”.

Let’s now apply this understanding of debt to the Australian property market.

Two types of buyers - owner-occupiers & investors.

Owner-occupiers are the purchasers of the property making a consumption decision.

They are more interested in enjoying the space, location, security and convenience owning a home offers someone.

Maybe they are a young family who is sick of moving from rental to rental and want to live somewhere where they can raise their kids.

Maybe they have pets and need some backyard space, or they have parents living with them and therefore need a much larger home.

These owner-occupiers are less concerned with the value of their property increasing or decreasing and more concerned about their living requirements and the utility a property offers them.

Therefore the “economic benefit” to this buyer can’t simply be measured by looking at cash flow or capital growth.

Instead, there are qualitative benefits that are sometimes hard to measure.

These people may see the value of their property decrease by 20% but not care because all of the reasons for purchasing the property in the first place are still intact.

These people may still see their purchase as a sound investment in their quality of life.

This is why when talking about Australian property prices, it is important to distinguish between the different types of buyers that are transacting in the marketplace.

The significance of all of this is that this type of buyer will be less likely to sell a property simply because the price has depreciated. The reason being, it is not all about FINANCES when it comes to buying.

In this instance, the debt used to purchase can be justified even if the servicing of a loan against that property starts to become expensive for the purchaser.

In summary:

The owner-occupier purchaser cares less about cash flow or capital growth.

The economic benefits to these buyers are focused more on qualitative measures from the utility their home offers.

Owner occupiers are less likely to sell their property even if interest rates increase.

Even if property prices decrease, they will view their debt as “good debt”.

How about the second type of buyer - the property investor.

The investor purchases property with only one thing in mind, to make a FINANCIAL return.

These returns can come by way of either:

positive cash flow through rental income or

Capital growth.

When measuring whether or not the debt is good or bad, the only consideration that needs to be made is whether or not either of the above is occurring.

First, let's look at the “positive cash flow” argument.

If a property investor purchases a $1,000,000 property and immediately leases it for $2,500 per month, the rental yield (before considering any ownership/maintenance costs) is ~3% per annum.

This doesn't sound like the worst investment idea in a world where interest rates on home loans are ~2% per annum.

Hypothetically investors could borrow the entire purchase amount and still collect a 1% rental income without any deposit...

In dollar terms, that would be the equivalent of making $10,000 per annum from a $0 investment.

With variable interest rates on mortgages now at ~3.5% (AND INCREASING), that same scenario where you borrow 100% of the purchase price results in a net rental yield of NEGATIVE 0.5%.

This means the same investor is now out of pocket $5,000 per annum on that same property.

In a rising interest rate environment, most property purchased between 2016-2022 would quickly fall into the “bad debt” category, where cashflows don't cover the cost of servicing interest repayments.

But what about capital growth?

If the value of that same property is increasing 10% per annum, the investor would (on paper) be making $100,000 per annum.

But what if capital growth is also in decline?

The latest data from CoreLogic shows that home prices in Sydney are down 4.3% from the peak and in Melbourne, down 2.8%.

NOW the investor is faced with rising interest rates, increased debt servicing costs and negative capital growth.

Again, the debt used to purchase by an investor is quickly defined as bad debt.

But what about if those investors start trying to sell?

Well, then everything works in reverse, and the negative feedback loop is set in place.

That feedback look goes like this:

Investors stop buying, creating less demand.

Less demand means lower prices.

Lower prices mean investors look to sell.

More selling creates more supply.

More supply creates lower prices, making everything worse.

When the loop is in motion, a scenario where accelerated property price falls becomes a reality.

In summary:

Investors purchase looking to make FINANCIAL returns.

Economic benefits to these buyers are - capital growth and rental income.

Interest rates rising decreases rental returns.

Interest rates rising also lead to price falls.

So why does “bad debt” matter?

Bad debt = Borrowed money that is used unproductively. Either in properties that are negatively geared or don't bring in any cashflows.

We think the Australian property market is approaching a point where a lot of the debt taken out between 2016 and 2022 will soon be considered “bad debt”.

So why should we care about any of this?

It is simple.

If the Australian property market is in a bubble, then we need to know whether or not the debt that acts as a foundation for the astronomical prices is either good or bad.

If the bulk of the debt can be classified as “good debt”, then prices are likely to be much more resilient.

If the bulk of the debt is “bad debt”, then the case for the bubble popping is much stronger.

Here is our take:

We think the market is very clearly in a bubble - Read our article here: Australian property in a drop?

We think the market fundamentals are laden with “Bad Debt” - We touch on this in today’s article.

This, in our minds, ends only in one way, with prices reversing and bottoming out only after a lot of the “bad debt” is taken out of the system, first through distressed sales and then defaults.