The bear case for negative gearing

The bear case for negative gearing

Get the taxpayer to pay for it

Negative gearing for a positive outcome…?

What’s on our mind: Negative gearing to cost taxpayers $6 billion? Property investors lose money, and the Australian taxpayer subsidises the losses.

What happened this week: Jerome Powell (US Federal reserve governor) thinks the US fed funds rate is going a lot higher, and it will mean “pain for some households and businesses.”

What are we watching next week: Aus building approvals data, Aus private sector credit data, US unemployment data

Prelude:

What’s on our mind:

The following headline published by Domain mostly inspired this week's ramblings.

The TLDR (summary) of that article:

The cost of negative gearing tax concessions is set to soar as interest rates rise.

Australian taxpayers will foot the bill to offset private landlords' lost income.

The cost to the public purse could rise to $6 billion. The last time it got this high was before the GFC in 2007-2008, when it peaked at around ~$9 billion.

Before we go any further, a quick reminder.

What is “Negative Gearing”?

In its most basic form, it is a tax concession offered to taxpayers, incentivising the acquisition and renting of residential property.

It ensures that investors who make a net loss renting a property out can deduct those losses against their personal incomes to reduce the tax they would need to pay.

The best way to illustrate this is with a hypothetical:

Investor A earns $100,000 per annum in personal income.

Investor A purchases a home for $500,000.

Investor A collects $10,000 per annum in rent. (INCOME = $10,000)

Investor A pays out $20,000 per annum in interest and other expenses related to owning the property. (EXPENSES = $20,000)

At a very high level (ignoring boring tax legislation), this person has made a loss from owning that property for that particular year of $10,000.

Investor A can now put this down as a tax deduction and, for tax purposes, would have a personal income of only $90,000.

Investor A then pays personal income tax on $90,000 instead of $100,000, paying less tax by making an investment loss…

So why did this get us thinking?

The simple answer is that the policy is a lose-lose situation for all Australians.

The investors because they make a loss renting out these properties.

The Australian taxpayer because they subsidise a portion of those losses.

The government because they collect less in taxes.

The less publicised and more damaging part of all this… billions of $ are being poured into loss-making investments instead of financing alternative productive investments.

The headline estimate of $6 billion for the financial year sounds terrible, but it got us thinking…

How much are the investors losing for it to cost the taxpayer $6 billion and how many of these “investors” are experiencing financial stress due to allocating a portion of their incomes to these loss-making properties?

If the cost to the taxpayer is $6 billion, this would mean investors are losing several billion $ more than this.

For example, if we assumed the average tax rate of all of these “investors” was ~30%, then the nominal losses by negatively geared investors across Australia would be a whopping $20 billion.

That is a lot of capital that could be financing investments that create jobs and increase economic productivity.

The lost opportunity:

We think negative gearing is the perfect example of a short-term approach to investing.

It provides economic stimulus by promoting demand for new housing (increasing economic activity through construction BUT, on the flip side, it locks in an investment in an asset that will produce nothing but losses and a drag on economic activity for decades to come.

We think this is the part of the policy that is severely under-appreciated. Think of it as a short-term sugar hit and the subsequent withdrawals… but this time over decades.

It encourages speculation in the property market, chasing loss-making assets instead of financing business investments that will increase economic activity, create jobs and improve Australia’s productivity for decades to come.

With capital growth in property prices in decline, these losses are now being compounded, and our sneaking suspicion is that the long-term consequences of the policy will start to rear their ugly head as interest rates continue rising.

Here is how it works:

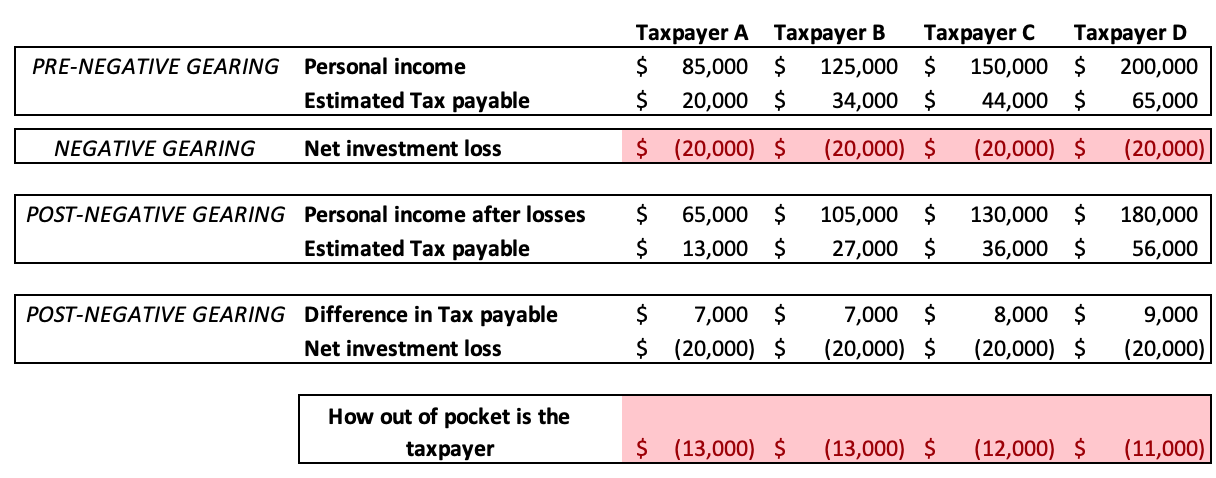

Negative gearing for four different taxpayers:

We need to preface this and clarify that we are not tax agents. There may be minor numerical errors in our spreadsheet below…

We took the ATO tax calculator and applied a personal income rate with no deductions, then reduced that same income by the losses to get our new figures.

Our calculations show that the people who benefit the least from negative gearing are the lower-income earners.

For example.

Someone earning $85,000 per annum with a $20,000 net loss from an investment property would still be out of pocket $13,000 (AFTER the tax concessions).

Someone earning $200,000 per annum with the same $20,000 net loss would be out of pocket $11,000.

The difference may only be $2,000, but as a percentage of someone's income, the person with the lower income is getting the short end of the stick.

We think this is the part of negatively gearing that is deeply misunderstood…

Most of the people we see that are negatively geared are the ones who can least afford it.

With property prices decreasing, the negative gearing equation doesn't stack up both from a taxation point of view and at the investment level.

Anyone considering putting themselves into a position where they are negatively geared should seek professional tax advice and try to understand what they are getting into.

Our emails are open to anyone that wants to get in touch.

Negative gearing - the least productive tax policy in the world?

Billions of $ are parked away in “investments” that generate yearly losses.

These “investments” create no new jobs and do nothing for economic productivity.

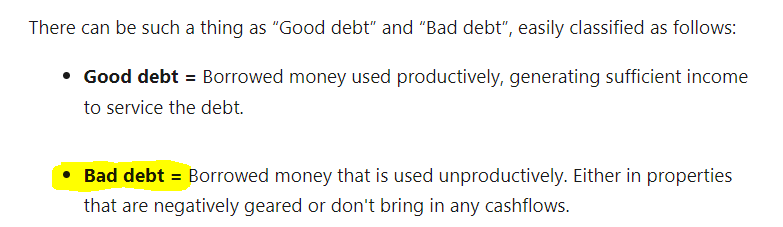

We touched on all of this in a previous article where we defined the difference between “good” and “bad” debt.

Check out that article by clicking on the image below.

Negative gearing encourages the worst debt and firmly sits inside our “bad debt” classification.

We also recommend everyone read the following article written by Dr Daniel Halliday, which touches on several other factors that make the policy hard to understand.

Property dashboard:

For those who are reading this blog for the first time, we just released a property dashboard where we put together a wrap-up of everything property across the NSW/VIC markets.

In our dashboard, you can find the following:

Our property data wrap for the week.

The feature article for the week

The chart of the week

Subscribe to get the email in your inbox every Tuesday/Wednesday evening.

To read our latest dashboard, click on the image below.

This should be required reading for all politicians on both sides of the fence and all Australians that care about the long term viability of the Australian economy and affordable housing. The abolishment of negative gearing should be a priority. Unfortunately, neither party is willing to take it up given what happened to Bill Shorten at the previous election. I still remember when houses were something that you simply lived in rather than part of your investment portfolio.