The Iceberg to your titanic

The Iceberg to your titanic

The coming fixed rate mortgage cliff

Higher rates for longer and a looming refinancing crisis.

What’s on our mind: Fixed rate mortgage cliff & “Talking Heads” on social media

What happened this week: US Inflation at 7.7%, RBA and the US Fed talking about slowing rate hikes.

What are we watching next week: Aus wage price index, Aus unemployment rate.

Prelude:

What’s on our mind:

The great Australian fixed rate mortgage cliff.

We can all see it coming but are we prepared and do we really get it?

Over the past few weeks we have started teeing big four bank exec’s come out and aggressively defend the strength of their balance sheets.

The narrative being pushed to the media is that the banks are well capitalised and the fixed rate mortgage rollovers will have little to no impact on business.

Some have even come out unprompted, which got us thinking… why the sudden need to aggressively spruik a strong balance sheet and why so publicly?

You only have to look back to the US Global Financial Crisis to understand why.

In 2008 the US housing market collapsed and brought about the GFC, the resulting collapse got so bad it put one of the USA’s biggest banks into bankruptcy (Lehman Brothers).

How did it happen?

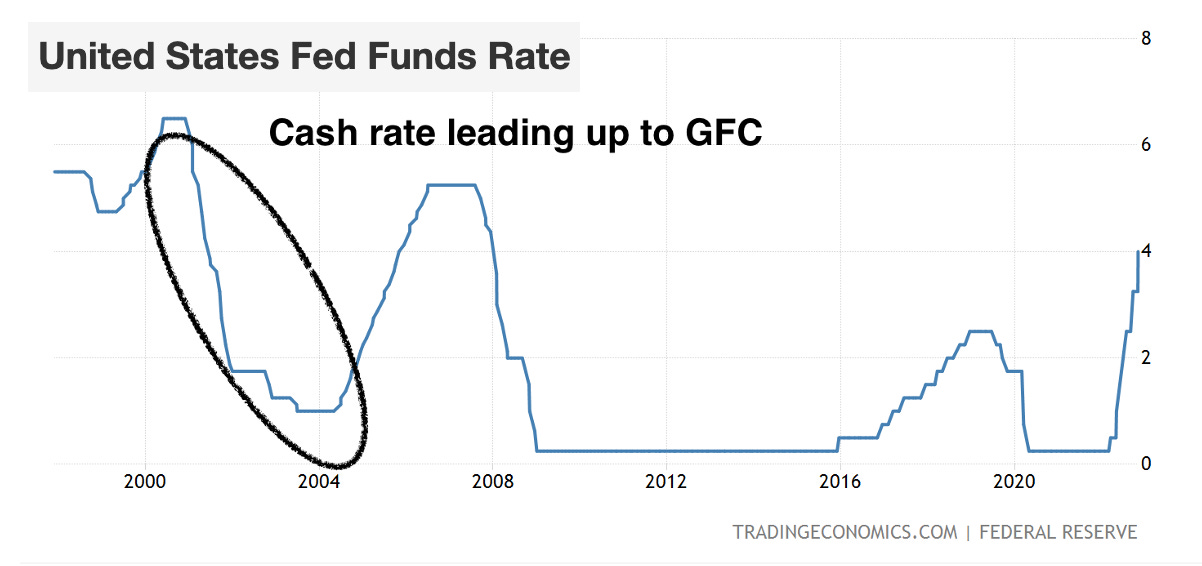

Through the early 2000’s property prices in the US were increasing - through to ~2007.

This was a result of rampant speculation by US property investors who took on more and more debt hoping that prices would continue going up. The aim was to buy, hold (sometimes renovate/develop) and flip for a quick profit.

All of this was made possible by the US Federal Reserve’s (US central bank) loose approach to monetary policy.

See the US cash rate through those boom years.

Then in 2007 the US Federal Reserve started responding to high inflation prints by increasing its cash rate - the result? A slowdown in the US real estate market.

Note* The 2007 slowdown in the US is an almost direct analogue to 2022 in Australia. The market doesn’t immediately collapse, instead price falls initially are relatively modest.

The consensus at the time was that the market would go through a small healthy correction and that prices would start to rise again - sound familiar?

One thing those people were missing was the massive fixed rate mortgage cliff looming for the US in 2008.

Just like we saw in Australia in 2020-2021, heaps of real estate speculators had amassed property empires by taking out mega loans - financed with initial fixed interest rates (teaser rates) well below market adjustable rates (variable rates).

For example, a borrower would take out a $1M loan with an initial 2 year interest rate of 2% per annum, which would then correct to the market adjustable rate of say 4 or 6% after that initial 2 year period.

Sounds awfully familiar again…

Unfortunately, those borrowers who could afford to pay the teaser rate’s couldnt afford to pay the adjustable rate.

This naturally led to delinquencies which led to foreclosures which led to what we now know as the Global Financial Crisis (GFC).

A US real estate collapse which almost took out entire global financial markets with it.

Now what is Australia facing?

Between now and the end of 2023 ~$158BN in fixed rate mortgages will be due to expire and require refinancing - normally a time where the interest rates revert to the current market rate.

Whilst some of these loans were written using 1.6-2% fixed rates, the market rates for mortgages are now at >5% - almost 3x higher than when the loan was first written.

In this scenario a borrower with $1M in debt is facing a cliff where the interest servicing burden could go from $16,000/annum to > $50,000/annum.

The worst part is the sheer size of the loans coming due - ~$158BN.

If we look at the lending data for the September quarter ($25.1BN) - the amount of fixed rate mortgages due to expire is ~six months worth of new loan commitments.

The question is - with the cash rate now back above 2014 levels will borrowers who purchased in the last 2-3 years absorb all of this refinancing?

Summarising all of this in the USA:

The US cash rate fell in the early 2000’s inflating a housing bubble.

Inflation started rising and the US Fed responded by increasing rates.

Increasing rates caused a collapse in the US housing market

US housing market collapse led to the Global Financial Crisis of 2008.

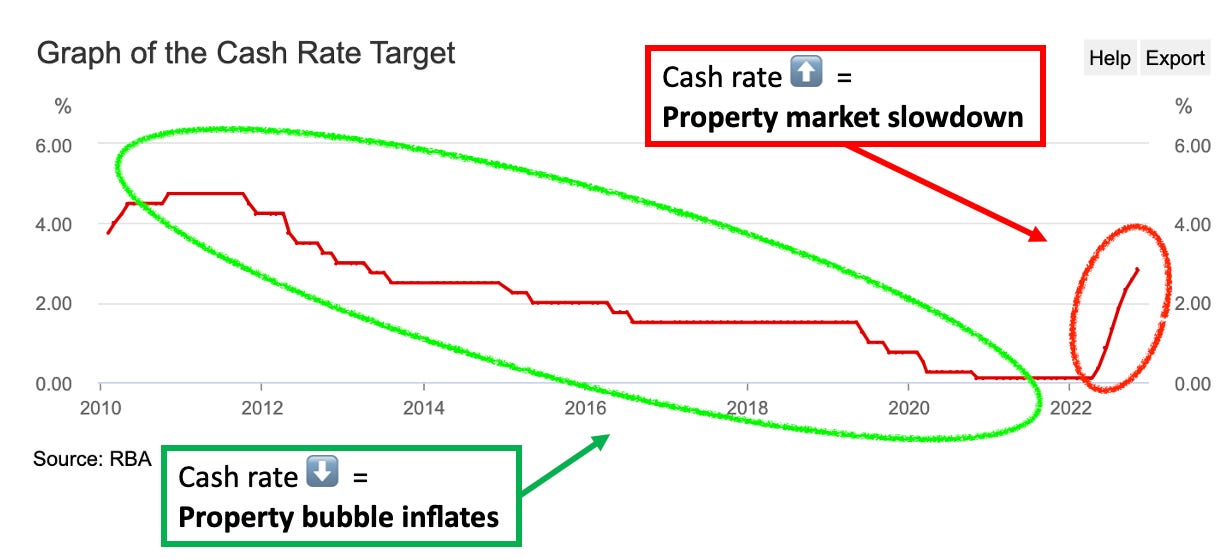

Now Australia?

AUS cash rates fell between 2018-2021, inflating a housing bubble.

Inflation is now rising and the RBA is responding by increasing rates.

Increasing rates HAVE caused a slowdown - will it cause a collapse?

What happens in 2023?

Now, we are not saying the same will happen in Australia.

Thanks to the boys and girls at the RBA who have extensively studied the Global Financial Crisis we hope they are more prepared than the US Fed was when everything was turned upside down in 2008.

The RBA even wrote a paper about it which you can read by clicking on the image below:

We will be watching and writing about everything as things develop.

Talking heads - 001

On a lighter note, today we are launching a new series to look forward to in future newsletters.

The series is called “Talking Heads”.

Here we will feature interesting hot takes we saw on social media during the week - of course, we will also provide some of our own commentary on the topic.

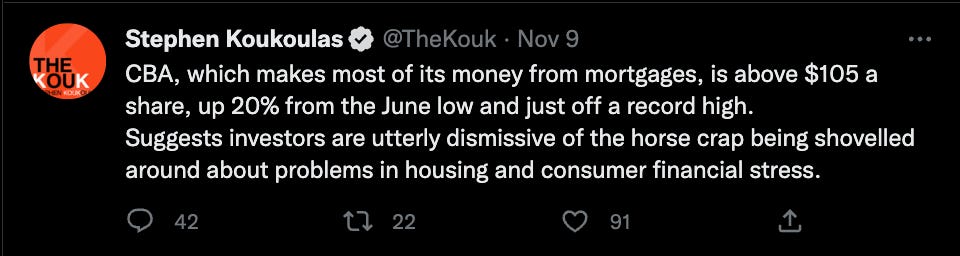

This week's hot take is from twitter's famous economist - Stephen Koukoulas.

This one made us laugh.

It seems @TheKouk has forgotten how bubbles work… it is the exact thing he is bragging about which makes a bubble.

An example of what we mean below is the share price chart for Bank of America leading up to the 2008 Global Financial Crisis (GFC).

Yep, it was trading at or near all-time highs and based on Kouk’s approach to macro analysis, the housing market in the US should have been rock solid.

Of course, it wasn't, and US house prices fell over 35% from the peak, and some of the banks with exposure to it went bankrupt.

Bank of America’s share price fell from ~US$55 all the way down to ~US$4 per share and if it weren't for government intervention it might not be around today.

Thanks for reading,

If you have anything you want to discuss feel free to DM us using the following channels:

On Twitter @Aus__Property

Via email at Auspropertymarket@gmail.com

Or through Substack - Property Down Under

Great one. Best article you've done so far- you kept it short and simple. No need to overthink this stuff