Property Dashboard

Property Dashboard

Everything you need to know this week

Property Dashboard - 10 August 2022

The feature article of the week:

Below is our feature article for this week’s edition of the newsletter.

This is the article we found most interesting to read, and the one we think is a “must-read” for all of our readers.

Key takeaways:

Co-founder of Judo Bank, Joseph Healy says he’s “paranoid about what could happen” as the RBA continue lifting the cash rate.

Healy describes the level of Australian household debt as “eye-watering”.

Healy warns, “We have a situation here where if interest rates move, as theory says they should, to deal with inflation, you have a huge problem in the household sector that will spill over into the SME economy,”.

Healy is quoted as saying “It is not the average borrower that brings the market down, it is the marginal borrower”.

Healy also said “I am nervous about the psyche that says, ‘she’ll be right, don’t worry about it. You are better being prepared for the worst and hoping it doesn’t happen, than saying ‘we don’t expect issues to emerge and we will all be OK.’”

Our Take:

The article is a look into the mind of a bank boss, someone who bankrolls the entire property industry. If he is worried, then so are we.

The quote that resonates most with us is, “it is not the average borrower that brings the market down, it is the marginal borrower”. This is something we think is being missed in almost all mainstream media and especially from the commentary the RBA/Treasury is making.

We think problems around the fringes are what cause a sector-wide collapse, and unless we recognise and acknowledge these possibilities, it will catch us all by surprise when it does happen.

To see a bank boss come out and speak so candidly is refreshing, though, and it does give us some hope that whatever the problems, we as a country will be able to work through them.

We are watching credit data to see how all of this unravels… watch this space.

Other Mainstream media 📰

High-end prices falling four times faster than average (AFR)

Sydney house prices tipped for sharpest fall in 30 years (AFR)

Nylex site among $150m of Caydon assets seized by receivers (AFR)

Australian house prices fall at 'fastest rate' since 2008 financial crisis (ABC)

Geelong building company Norris Construction Group collapsed owing $27m (News.com.au)

Why should you care:

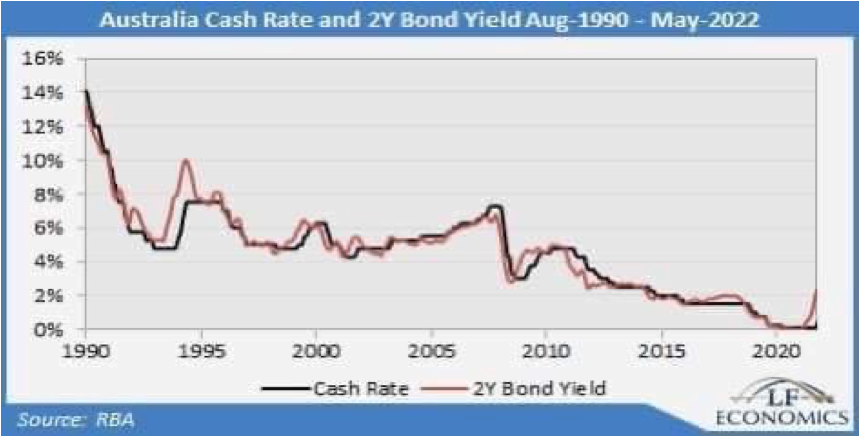

The black line above represents the RBA cash rate.

The red line above represents the 2-year government bond yield.

We have found that there is a positive correlation between the cash rate and 2-year bond yield, where the cash rate lags the yield % by six months.

Our takeaway:

The 2-year Australian government bond yield currently trades at ~2.4%.

Our prediction is that the 2-year bond yield has started to top out and is finding a long-term base.

We expect the RBA cash rate to move into a range somewhere between 2.25 and 2.75%.

This leaves the RBA stuck between a rock and a hard place where inflation is almost 3x the RBA cash rate. Our internal view is that it is more likely the inflation rate comes down to meet the cash rate than the opposite happening.

Our expectation:

We expect the RBA cash rate to move up into a range of 2.25 to 2.75%, where it will start to trade sideways.

Given that the cash rate is currently at 1.85%, that should mean we see another 0.5-1% in rate hikes before the RBA starts to slow down the pace of its rate hikes or stop all together.

It would be great to add an estimate of PPOR vs IP to the listing statistics, even if only a rough estimate based on relatively higher IP prevalence in units.