Investing in property

when rates are high

Is now a good time to invest in property?

What’s on our mind: Can you invest in property when interest rates are high? What are the best ways to go about it? This week we look at three different approaches and pick our favourite.

What happened this week: Australia’s inflation rate hit 6%.

What’s coming up: RBA cash rate decision on Tuesday at 2:30pm AEDT.

Prelude:

What’s on our mind:

Residential property is Australia’s most popular investment class.

The value of all Australian residential property peaked at just under $11 trillion in mid-2022, making it the single biggest asset class in Australia.

For some context - the Australian gross domestic product (GDP) sits at ~$2.2 trillion.

But what are the most common ways to invest in property, and which approach makes sense in the current high-interest rate environment?

Today we look at three different ways to invest in residential property & how the approaches stack up in today’s market environment:

Three ways to invest in property:

The three main ways to invest are:

Investing through property development (Short term) - This combines income and capital growth but involves turning over projects much quicker and locking in profits along the way.

Invest for income (Medium-Long term) - This is where the investor will buy a property that pays out more in rent than it costs to own/maintain. The goal here is to build a retirement income through property.

Invest for capital growth (Long term) - This is where an investor buys property with no intention to sell in the short-term, instead hoping that the property's value appreciates so that it can be sold later.

All three approaches can make sense if implemented correctly, BUT not all work in high-interest-rate environments.

Investing in property development:

This is where an investor purchases an existing property or parcel of land to build on it and sell it for a profit.

The process is relatively complex but can be boiled down to three main stages:

Design stage - The investor (developer) engages an architect and creates a design compliant with the local council’s zoning requirements. This stage typically takes >2 months to complete, depending on how many consultants need to be engaged and the complexity of the design.

Town planning approvals - This is where the investor (developer) needs to go through the local council and get approvals for the proposed development. This process typically takes ~12-18 months, assuming no hidden issues and a simple design.

Construction stage - This is where the investor (developer) engages a builder and gets the approved design built. This can take upwards of 12-18 months to complete and is often the hardest to navigate.

(Source)

Property developers are ultimately in the business of turning over projects.

Once built, the developer only holds onto the properties briefly. They then sell the developed properties and recycle the profits into a new project.

The typical time a developer spends purchasing and developing a project can range from 12-36 months, depending on how big the project is.

A single home can be completed in under 12 months, whereas a development with eight units might take 2-3 years.

Property development when interest rates are high:

Property developers only hold onto a project for 12-36 months, so this investing approach can work even when interest rates are high.

When purchasing a new site, the developer will account for the increased interest costs and any potential changes to the sale price of the units being developed in the project feasibility study.

The feasibility study is done BEFORE purchasing a site meaning the developer can adjust the price they are willing to pay to make the financials stack up.

Ultimately, property development, when interest rates are high, can still be profitable.

It just means the developers must be more diligent with the feasibility studies BEFORE purchasing.

What we are doing right now:

We are actively looking for properties we think have development potential.

We expect property prices to fall over the next 6-9 months and hope to see some opportunities to buy between now and Q2 2024.

Subscribe to see some of the feasibility studies we will do on properties we look at over the coming months (below is a snippet from one we did a while back):

Property investment for income:

This is where an investor buys a property and rents it out for passive income.

The emphasis of this approach is to try and collect more rent than the costs of owning and maintaining a property.

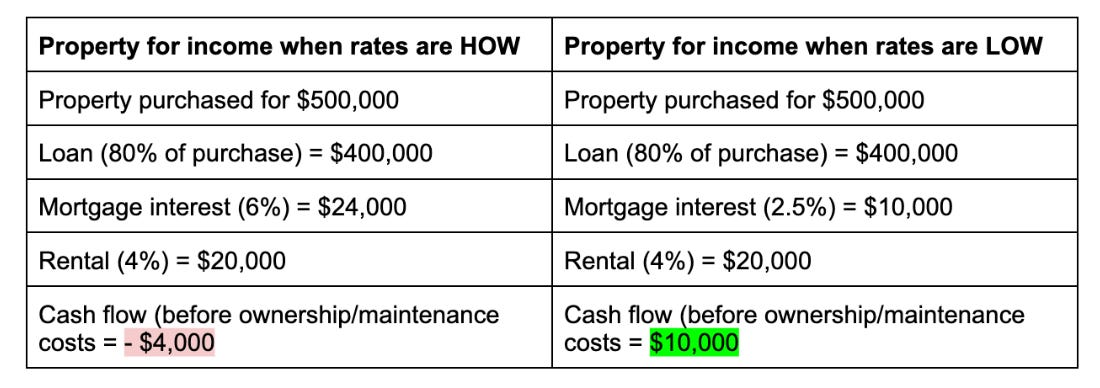

Property investment for income when interest rates are high:

This approach stops working when interest rates go up.

Average rental yields across Sydney and Melbourne range from 2-5%.

At the same time, mortgage interest rates are at or above 6%, meaning the cost of borrowing money is much higher than the rental yields on a typical residential property.

A worked example:

Most investors will argue the property increases in price, and so the capital growth offsets the losses (when rates are high), BUT if an investor has a portfolio of these properties all losing money, it can force them to start selling some to pay off debts.

This approach doesn't stack up in a high-interest rate environment because many other investment opportunities can give investors income without the risks/costs associated with property ownership.

For example:

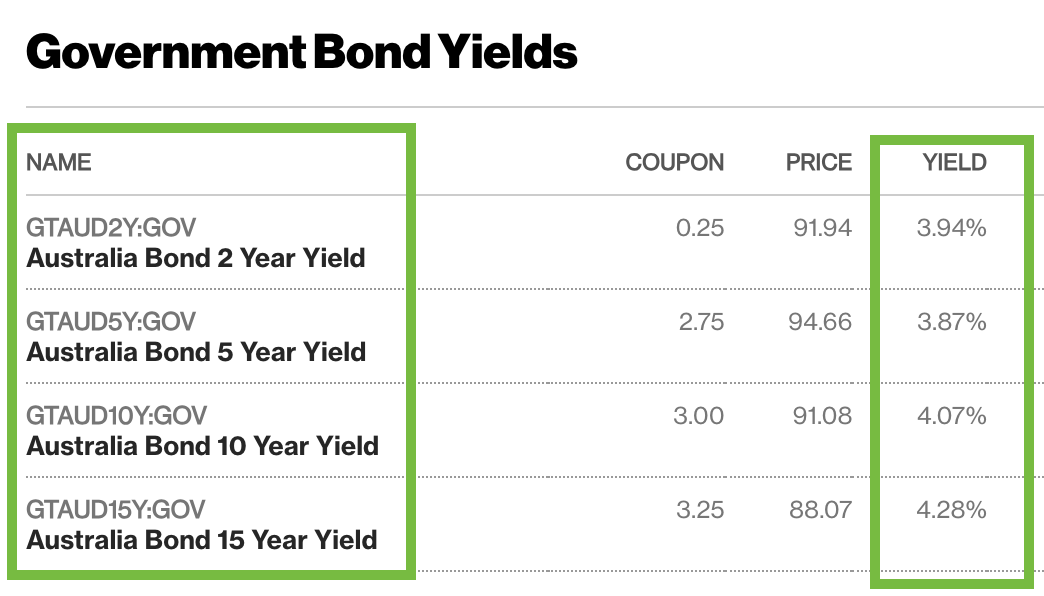

REITs (Real Estate Investment Trusts) yield >7% - almost double residential property yields.

Government bonds (considered “risk-free”) yield between 4% and 5%.

(Source)

Without getting too technical, residential property for income isn't an efficient way of investing money in a high-interest rate environment because there are far higher yields in different asset classes.

It especially doesn't work when the cost to borrow money is higher than rental yields.

What we are doing right now:

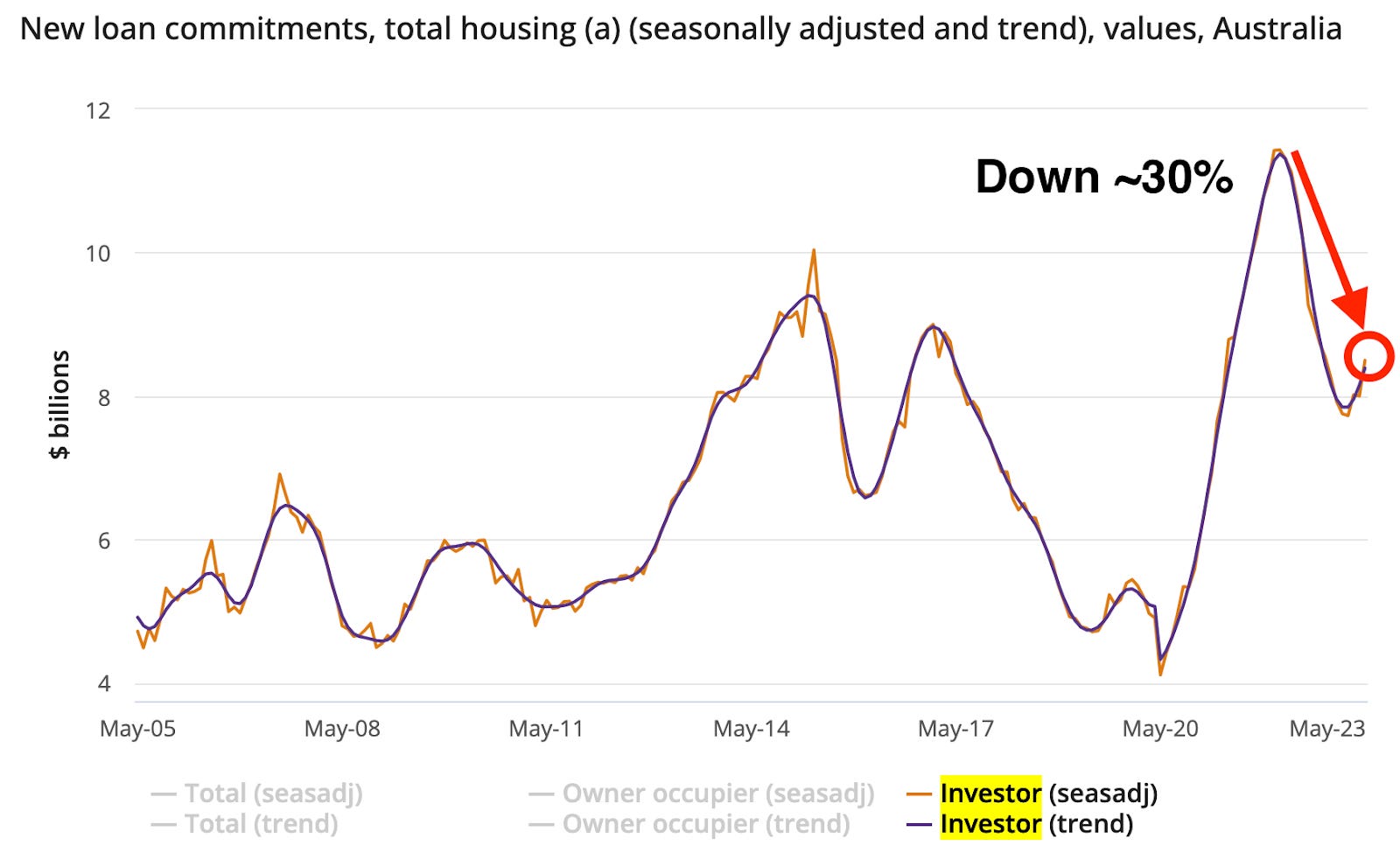

We are already seeing investor buying of property almost disappear.

For context, investor lending for new purchases is down almost ~30% from its peak.

(Source)

We are looking for significant discounts on investor-friendly units/townhouses.

We are primarily focused on suburbs across Melbourne and Sydney which we think:

Offer the best chance of future capital growth, and

CURRENT rental yields >5.5%.

Currently, these opportunities are almost nonexistent in Sydney and are hard but not impossible to find in Melbourne.

Investing for capital growth:

This is where an investor buys the property and waits for its value to increase over time.

Often, an investor buys a property in a suburb that isn’t yet fully developed.

The investor buys a large plot of land or a house on a large block and waits for urban sprawl to do its thing.

In 10-15 years, when the suburb is more developed, there are more schools, more parks, and more shopping centres in the area, the value of the property goes up, and the investor's large block of land is worth a lot more than the initial purchase price.

Investing for capital growth when interest rates are high:

This approach can still work when interest rates are high, but the time it takes for a property’s value to appreciate can take much longer.

When interest rates increase, development activity starts to slow, projects are put on hold, and developments in areas requiring investment are halted.

What we are doing right now:

This is the area we are least interested in at the moment.

With interest rates high, the cost of holding a property is naturally higher than we would want for this type of investment approach.

We plan to re-consider long-term land banking opportunities IF/When property prices fall.

Currently, prices in the suburbs with long-term capital growth potential are far too high.

Thanks for reading,

Aus_Prop team.

You can contact us here:

On Twitter @Aus__Property

Via email at Auspropertymarket@gmail.co

Or through Substack - Property Down Under

Thanks again for a great piece. I think the example of cashflow from a property investment is incomplete without stating the approximate management/ repair/ taxes. This really eats into cashflow further. This is little understood by the public.

What are your thoughts on Japan 2.0 circa 1989 onwards??