How to prop up property prices..

How to prop up property prices..

just another day in the office

How stamp duty reforms will impact property prices

What’s on our mind: The NSW government recently announced new “stamp duty reforms”, but what impact will this have on property prices?

What happened last week:

AUD/USD trading at 68c off the back off commodity price falls.

Retail sales stronger than expected up 0.9% month to month vs a forecast of 0.3%.

Quotes from US Fed chair Jerome Powell this week:

“We got supply-side timing issues wrong”

“Economy can withstand monetary policy moves”

What are we watching this week:

Melbourne Institute Inflation gauge (04.07.2022)

Credit data - lending indicators for May (04.07.2022)

RBA cash rate decision & statement (05.07.2022)

Prelude:

What’s on our mind:

Our inspiration for today’s note was the following quote:

“The nine most terrifying words in the English language are: I'm from the Government, and I'm here to help."

With that in mind, let's get into it.

First, what is stamp duty?

Before we get into the proposed stamp duty reforms, we should first establish what stamp duty is and how we pay it?

Keeping everything very high level, stamp duty is a tax paid to the state governments at the time of every property transaction.

Stamp duty is paid by the purchaser, with the amount changing depending on the property being purchased.

This means the higher the purchase price, the higher the stamp duty that must be paid.

By way of an example:

A first home buyer paying $1,500,000 for a property in NSW would have to pay the government $66,700 in stamp duty taxes.

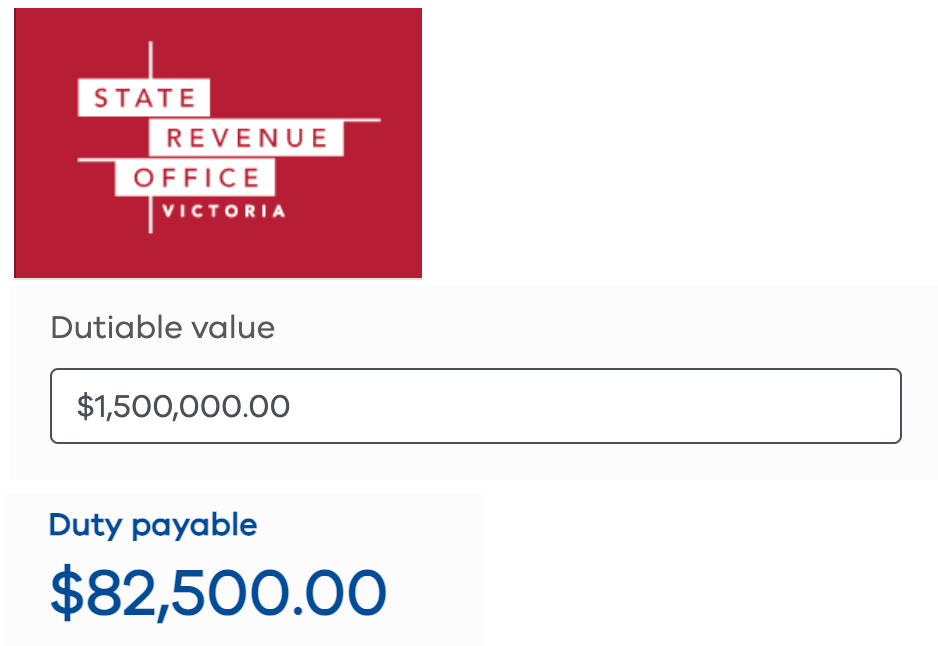

A first home buyer paying $1,500,000 for a property in VIC would have to pay the government $82,500 in stamp duty taxes.

A ~4.4% tax in NSW and a ~5.5% tax in VIC are paid directly to the government.

Most important, however, is the timing of this payment.

Stamp duty is paid UPFRONT, meaning that a purchaser needs to be able to make a cash payment of this amount to the government when settling on the property.

A purchaser cannot take out a loan to fund this portion of the purchase, meaning they will need to pay for it with cold hard savings.

To summarise:

Stamp duty is a ~4.4% (NSW) to ~5.5% (VIC) tax that a property purchaser pays to the respective state government UPFRONT when settling on a property.

The key word here is - UPFRONT.

So what is stamp duty reform?

The idea of getting rid of stamp duty on property transactions isn't anything new.

State governments have thought about it in the past, but the blocker has always been the dilemma of giving up upfront tax revenue and exchanging it for tax revenue paid to the government in the future.

Basically, a decision where the government decides whether it wants to inflict short-term pain on tax revenues in favour of long-term gains.

This is mainly because scrapping stamp duty taxes would decrease the state government’s upfront tax revenues on property transactions in favour of a smaller, regular, recurring annual tax.

The NSW government has made the first move and, as part of its 2022-23 Budget, announced that first home buyers purchasing properties up to $1.5 million will be provided with the option to pay an annual property tax instead of transfer duty.

NSW premier Dominic Perrottet said that removing the stamp duty tax would increase the prospects for first home buyers entering the property market, saying that stamp duty “is one of the largest upfront costs to buying a home” and that replacing it with an annual property tax would increase affordability.

The NSW government added to this rhetoric by saying that stamp duty taxes added two years to the time required to save for a home deposit.

So the policy is being marketed as something that would improve housing affordability (we disagree).

So the main selling points for removing the stamp duty tax is that it will:

Help first home buyers take a step onto the property ladder.

Decrease the time required to save a deposit for a home and improve affordability.

So what is the NSW government proposing?

The reforms would give first-home buyers the CHOICE to pick either one of the following options:

To pay the standard stamp duty taxes applicable at the moment.

To pay NO stamp duty, but opt-in for an annual tax payment equal to $400 + 0.3% of the land value of the property.

The option to choose would be capped on properties valued up to $1,500,000.

It's also worth noting that property tax legislation still needs to pass the NSW parliament, which is not in place in NSW (before you go out and buy based on this article).

Perrottet and the NSW treasurer, Matt Kean, said it would be introduced in the second half of 2022, with eligible first homebuyers able to apply from 16 January 2023.

Now, a hypothetical scenario where a first home buyer purchases a $1,500,000 property.

The block of land is valued at $1,000,000 and the building at $500,000:

If the first home buyer chooses to pay the stamp duty tax UPFRONT, they would be out of pocket a total of $66,700.

If a first home buyer opts in for the annual property tax, they would pay NO upfront stamp duty and instead pay $3,400 ($400 + (0.3% of $1,000,000)) for every year they own the property.

With that difference, the stamp duty represents almost 20x the annual tax payment.

In this hypothetical scenario, first home buyers pay NO upfront stamp duty and get to keep the almost $66,700 in savings they had built up over several years.

So how will stamp duty reform impact property prices?

The answer to this question is simple and is directly related to the $66,700 in stamp duty taxes that a first home buyer won't need to pay.

The high-level summary of a property purchase is as follows:

A buyer would save up a 10-20% deposit and decide to buy a property.

On the settlement date, the buyer would then pay the deposit + stamp duty taxes.

The best way to illustrate the difference is by running through a hypothetical purchase scenario:

This time the first home buyer is paying $1,500,000 and has a 10% deposit.

The buyer would save $150,000 and purchase the property.

The buyer would pay $150,000 + $66,700 in stamp duty taxes on the settlement date.

The total amount of savings a first home buyer would need to be able to make that purchase would be $216,700.

Now, let's run through the same hypothetical scenario with the stamp duty reforms in place:

This time the first home buyer is paying $1,500,000 and has a 10% deposit. The buyer opts for an annual property tax instead of the stamp duty.

The buyer would save $150,000 and purchase the property.

The buyer would pay $150,000 + $0 in stamp duty taxes on the settlement date.

The total amount of savings a first home buyer would need to be able to make that purchase would be $150,000.

By opting for the annual tax payment, the first home buyer would be buying a more expensive property with ~30% less in savings.

Another illustration, under the old system:

A first home buyer with $150,000 in savings who is putting down a 10% deposit can afford a property valued at ~$1,000,000.

Split via a 10% deposit = $100,000 and stamp duty taxes of ~$40,000.

Under the new system:

That same person would just pay a 10% deposit on a $1,500,000 property.

With the policy change, first home buyers purchasing power would increase by $500,000 (50%).

*All of these calculations ignore borrowing power, legal fees or other factors that should be considered when considering property transactions. We are just trying to illustrate the reforms' impact, not running a settlement calculation.

Bringing everything together:

It is simple.

Less cash is paid to the government upfront.

That cash saved is then put towards a bigger deposit on more expensive property.

For a person with $150,000 in savings.

If stamp duty needs to be paid, $150,000 buys you a $1,000,000 property and settles ~$40,000 in stamp duty taxes.

If the stamp duty tax is gone, that same buyer has enough for a 10% deposit on a $1,500,000 property.

An increase in buying power of almost $500,000 (50%).

We think this ultimately leads to increased demand for properties in the <$1.5M market.

Sales from owners in this market will then look to upgrade, which will feed into more demand for more expensive properties.

So is this policy more about tackling the affordability crisis, or is it just another “throw the kitchen sink at it” moment by policymakers to prop up the property market.

We have our views on it all...

As you say, you haven't accounted for their reduced borrowing capacity with the land tax, which is somewhat significant. But yes, its a complete sham designed to put a floor under prices.