Get rich quick property scheme

Get rich quick property scheme

gone wrong

When spruiking goes wrong

What’s on our mind: Is property the most spruiked asset class in Australia? We think so. Read on to see our take on what these spruikers take as gospel.

What happened this week: RBA rate rise by 0.5% (More on this at the end of today’s article).

What are we watching next week: New Zealand cash rate decision, Canadian cash rate decision, Australian unemployment numbers and US consumer price index data.

Prelude:

What’s on our mind:

This week’s article is dedicated to all the property spruikers out there.

Those who are parading as “investment strategists”, “financial independence gurus”, “property investment specialists”, and whatever else they call their spruiking selves.

These people can be found in the paper, in ads between youtube clips and all over social media.

They all preach a similar pathway to financial independence through property investment.

The process goes a little bit like this:

Step 1) The investor is encouraged to buy a property with as little a deposit as possible.

(Encouraging the buyer to take on as much leverage as possible)

Step 2) Refinance the property at a higher valuation and take out the “equity”.

(Encouraging the buyer to take out even more leverage, this time disguised as “equity”).

Step 3) Take that “equity” and go and buy a second investment property.

(Using the “equity” AKA debt to purchase another property, encouraging even more debt)

Step 4) The final step is to go back to step 2 and repeat the process continuously until you have amassed several properties.

They tell you that investors can achieve “financial independence” by rinsing and repeating this process.

The underlying premise is that by using “other people's money”, you can take a modest amount of cash and turn it into a property fortune.

After all this is done, the investor is encouraged to hold the properties for as long as possible, letting the capital growth part of the process inflate the debt away.

The longer you hold, the more money you make (or so they claim).

What they forget to tell you about is what happens if there is no capital growth or (god forbid) negative capital growth.

With interest rates increasing, we think it's the perfect time to run through a hypothetical scenario where these conveniently avoided topics become a reality.

Scenario 1: No capital growth

Step 1)

The investor takes $50,000 and purchases a property for $500,000, taking out a $450,00 loan.

Step 2)

Three months and some minor renovations later, the investor is encouraged to refinance the property and take out of the property $100,000 as “equity”. The investor now has a loan amounting to $550,000.

Just like that, the investor has unlocked $100,000 in cold hard cash (forget about the debt).

Step 3)

Now you take that cash and purchase a second property for $1,000,000, using the cash as a deposit.

The investor is now left with a loan amounting to $900,000 against the new purchase.

The investor is now in a position where they own one property with a $550,000 loan and another with a $900,000 loan.

Step 4)

The final step of the process is to repeat steps two and three.

The investor now goes back to step 2 and repeats the process continuously with the aim of purchasing as many properties as quickly as possible.

For the sake of today’s article, let's keep it simple and stay at two properties.

You have managed to take $50,000 of cash and turn it into a $1,500,000 property empire.

The cost to purchase these two properties is as follows:

Property 1= $500,000 and property 2 = $1,000,000.

Against that empire, you hold loans totalling $1,450,000.

The property spruiker will now tell you that property prices double every ten years, so all you need to do is wait and let the capital growth inflate away your debt.

Assuming the spruiker is correct, an investor should expect to see property prices rise by 10%/annum.

The value of the investor's portfolio in 12 months’ time should therefore sit at $1,650,000.

In that scenario, the investor's net worth increases from $50,000 to $200,000, almost 4X what the investor put in.

Returns that are almost too good to be true…

But what if there is 0% capital growth?

A year has passed, mortgage rates are increasing, and your property portfolio’s valuation is unchanged.

Your net worth is unchanged. You still have $1,450,000 in debt and a property portfolio valued at $1,500,000.

Maybe the rental income covers the investor's interest repayments, or the investor has a day job that helps cushion the blow of high ownership costs.

This scenario is not the end of the world.

The investor will do everything they can to try and hold onto their property portfolio, anchored to the belief that eventually, they will see those sweet, sweet 10%/annum capital gains and financial independence that follows.

Now, what happens when we get negative capital growth?

Scenario 2: -10% Capital growth

Now, let's run the same scenario back.

The investor takes that $50,000 and turns it into a $1,500,000 property portfolio against which they have $1,450,000 in debt.

After the first 12 months of ownership, the investor realises the RBA has increased cash rates by 1%, and property prices are down 10% across the board.

The investor's property portfolio is impacted by the price falls, with neighbouring properties selling for far less than what the investor paid for theirs.

The investor is now faced with the reality of a portfolio worth 10% less on paper.

The property portfolio is worth $1,350,000, but the investor's debt stays the SAME at $1,450,000.

The investor now finds themselves in a NEGATIVE EQUITY position of - $100,000.

All of a sudden, the portfolio of properties is not only costing the investor in terms of monthly negative cashflows, but they are also delivering capital losses.

This double whammy of losses viciously reduces the investor's net worth.

This is the issue with leverage (debt). It works spectacularly in both ways.

If the price of the leveraged asset increases, it can produce incredible riches.

If it works against an investor, it can wipe them out completely.

This is the side of the hustle these spruikers won't tell you about, and if you mention it, they will most likely start talking down to you as if you don't understand the strategy.

They will almost always refer to the last 30 years of capital growth and explain how that past performance is an indicator of what could be expected in the future.

Anyone with any financial literacy knows this is never the case with any investment.

What does this mean?

This is why the property market is so fragile going into an RBA rate hike cycle.

2020 and 2021 saw these spruikers go into overdrive, marketing themselves and their strategies.

We suspect many people took advantage of record-low interest rates and followed these spruikers into these debt-induced buying sprees.

With interest rates heading higher and property prices starting to fall, we suspect these people will be just as quick to start selling their highly levered properties.

All of this accelerates the losses in the space and starts a vicious cycle of prices falling, encouraging more selling, leading to prices falling even more.

Finally, what does this week's RBA rate hike change?

We touched on the impacts RBA rate hikes have on lending rates and how we think that feeds into property prices in a previous article which you can read here: What causes mortgage rate increases?

The key takeaway was how we try to forecast forward mortgage rates based on banks funding costs.

After all, if we can try and predict where we think mortgage rates will be at any point in the future, we can have a good idea of whether it's the right time to hold leveraged assets (Property) or not.

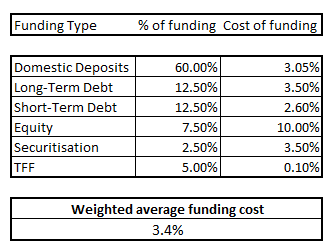

Our formula was as follows:

(1) Funding costs x% + (2) Net interest margin y% = (3) Mortgage rates z%

We determined that the long-run average net interest margin for banks was 2.25% and used the following table to work out funding costs at 2.4% using current figures for all of the below:

Plugging in the RBA cash rate, we get lending rates of:

(1) Funding costs 2.4% + (2) Net interest margin 2.25% = (3) Mortgage rates 4.65%

Something to note:

We saw CBA and Westpac offer 2-2.5% term deposit rates.

Given the RBA cash rate is so closely tied to term deposit rates. Clearly, the banks think the cash rate is headed much higher and are trying to lock in short-term funding at these rates.

So what is the market telling us?

That's right. The markets think the cash rate will be at 3.05% in December.

Plugging this into our table, we get the following value for funding costs:

Now going back to our formula, we get a forecast variable home loan rate for December as follows:

(1) Funding costs 3.4% + (2) Net interest margin 2.25% = (3) Mortgage rates 5.65%

How exciting does a 2.5% yielding property in the inner suburbs of Sydney or Melbourne sound with mortgage rates at those levels?

We think the answer to this question is pretty obvious.

I’m not a spruiker, but a homeowner and couldn’t care less if valuation fell since I have zero mortgage stress and don’t factor in home equity in my own financial decision making. In fact I’d welcome it price falls. But in your example, 1. Lenders won’t be willing to lend further if you’re already so indebted so in example of property #2, it’s not gonna happen and 2. Prices double in ten years implies annual growth of roughly 7.2% - rule of 72, not 10%.

This article largely applies to the most recent buyers at peak prices and doesn’t allow for rising rents and support from negative gearing tax breaks. The direction of the article is somewhat correct but overstated. There will be hard times for some but there are plenty,like me with fat stacks of super and previous property equity (15% down? Still equity rich) ready to come in when the numbers improve and interest rates turn the corner. Thus there will be a floor placed under the ‘crisis’ scenarios portrayed in articles like this.