Canadian property prices down ~26% - SYD/MELB next?

Canadian property prices down ~26% - SYD/MELB next?

The world's declared a rates war.

Canadian real estate down ~26% - Can the same happen in Sydney & Melbourne?

What’s on our mind: Canadian property prices falling off a cliff. Sydney and Melbourne immune? We thought we could interview a Toronto-based agent to try to find an answer.

What happened this week: Reserve Bank of Aus raised rates by 0.5%, the Canadian central bank raised rates by 0.75% and the European central bank raised rates by 0.75%.

What are we watching next week: US inflation rate, Australian unemployment statistics.

Prelude:

What’s on our mind:

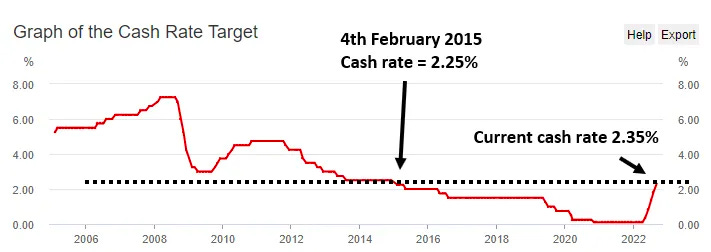

The big news this week in Australia was the increase in the cash rate to 2.35% the highest level since Feb-2015.

So far, CoreLogic data shows that cash rate increases leading to a fall in prices in Sydney by 7.3% and by 4.3% in Melbourne.

We have argued multiple times that it is less about the number and more about the RELATIVE level of the cash rate.

To try and illustrate our point today we will focus on what is happening in Canada right now.

Why should we care about what's happening in Canada?

Because this week, the Canadian central bank also increased its cash rate.

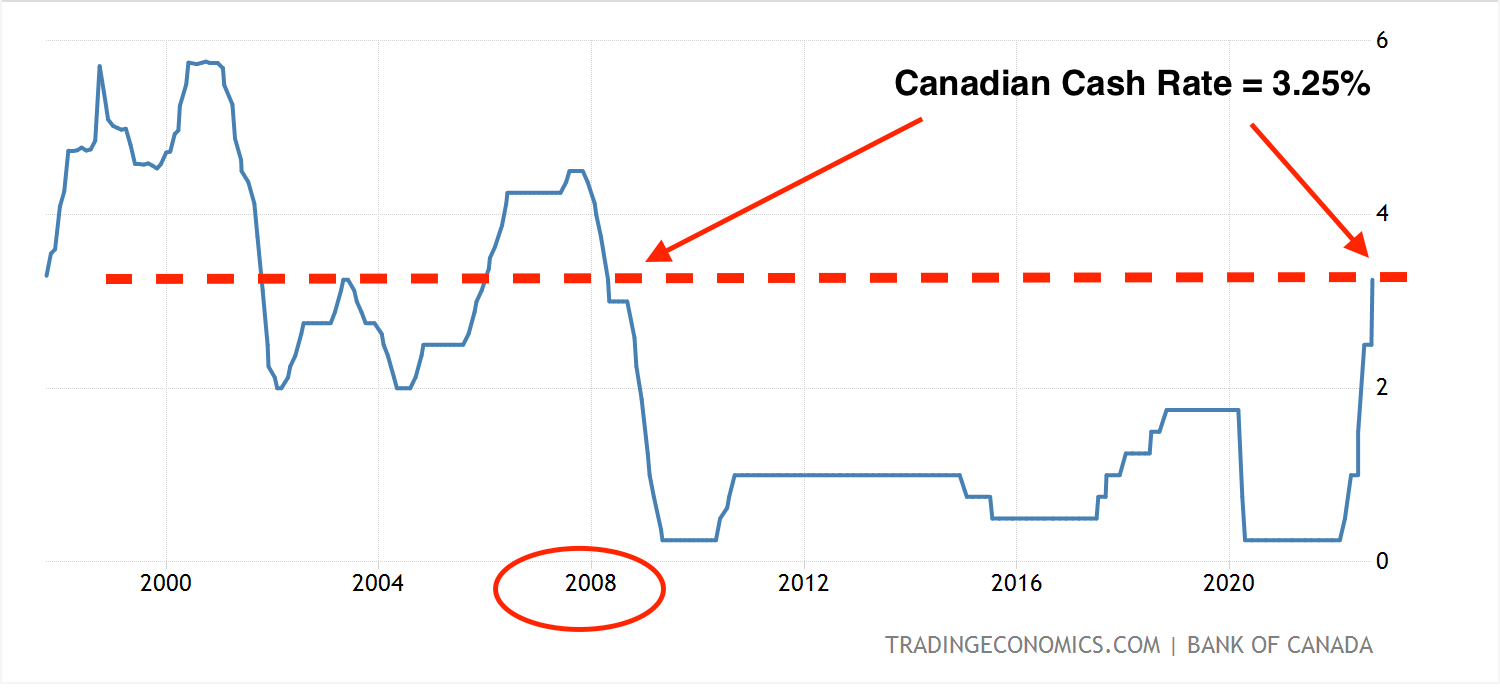

The main point of difference, though is that the Canadians took their cash rate to the highest level since the global financial crisis (GFC) in 2008 to 3.25%.

The decision by The Bank of Canada to raise the cash rate by 0.75% came with a warning that rates will continue increasing until inflation is under control.

Since the Canadians started raising rates, property prices across Vancouver and Toronto are down up to ~26%.

So why have prices fallen so much more in Canada than they have in Australia?

It is because everything is relative.

The Canadians started raising rates a lot earlier than the RBA did in Australia and quickly reached unprecedented levels.

Right now the RBA has its cash rate at 2015 levels, the Canadians got to 2015 levels back in April after just two hikes.

The RBA is now 2-3 rate hikes away from 2009 levels which might mean that by Christmas, Australian property market will be operating in a borrowing cost environment not seen since 2009.

So property prices in Canada’s two major cities are down by upto 26%...

The natural questions then become:

Could the same thing happen across the Sydney and Melbourne markets?

ANDAre there any similarities between the Australian and Canadian property markets?

To try and answer these questions, we asked ten questions to Toronto-based (Canadian) real estate veteran - Gina Athanasiou.

Gina has been in the industry since the early 1990s and has been actively buying and selling real estate since 2005.

Gina is slightly different from the typical real estate agent because she comes from a science background. This uniquely positions her to bring a more analytical approach to assessing the state of real estate markets. (this is refreshing to see)

She works mainly in the Downtown Toronto market.

Her primary client base is end users of property and family buyers looking to settle down.

One thing that stuck with us whilst we were putting this together was the following quote from Gina, and we couldn't agree more with what she had to say.

“I’ve seen my fair share of crazy in the last 17 years, but this time it’s different….”

With that, let's get into the interview.

Our interview with Gina Athanasiou

Take us back to 2019. How was the Canadian property market behaving before the pandemic?

Gina’s answer:

In 2017 the Canadian government attempted to slow the growth in home prices by introducing various measures like “mortgage stress testing” and various other provincial-led initiatives.

This made it more difficult to borrow and, naturally, impacted property prices.

Prices were down ~18.9% across Toronto from 2017 to January 2019.

By 2019 average Canadian real estate prices had not recovered from the 2017 downturn.

Our take:

This sounded awfully familiar to the royal commission-led firming up lending standards across Australia.

In almost identical fashion to the Canadian market, From the end of 2017 to the end of June 2019, Sydney property prices were down ~12% and Melbourne prices down ~10%.

How about 2020 during and immediately after the pandemic struck?

Gina’s answer:

In the first few months of 2020, right before the first lockdown was announced, the Toronto real estate market was running quite hot as it usually does in the first months of every year due to the seasonal lack of inventory.

As soon as the first lockdown was announced, the market died. Buyers and sellers were extremely fearful. It was basically just crickets everywhere.

That lasted for 2-3 months.

Our take:

Again awfully similar to Australia, where lending basically froze.

The Reserve Bank of Australia (RBA) was so worried that it even considered calling for a pause on property transactions to avoid a panic in the property market.

It sounds to us like the Canadians experienced the same thing.

What was the Canadian government's response to COVID, and what impact did it have on property prices?

Gina’s answer:

The Bank of Canada responded by slashing its equivalent of a cash rate rate from 1.75% to 0.25%.

The aim was to try and stimulate the economy and to try and unfreeze the lending markets.

Our take:

The exact same response as the RBA, which reduced its cash rate to the lowest level in history - 0.1%.

What were credit conditions like in 2021, and how are they different now? (i.e. how easy was it for someone earning $100,000 to borrow money to buy a property.)

Gina’s answer:

Incomes didn't change in any significant way year over year.

The cut in interest rates did, however impact the borrowing power of buyers, increasing the amount banks were willing to lend significantly.

This, combined with low inventory levels (because people didn't want to sell during COVID lockdowns & prices were going up) created a perfect storm for housing prices to skyrocket in areas like Vancouver and the downtown Toronto area.

Our take:

Again a direct analogue of Sydney/Melbourne.

Almost limitless lending from the banks coupled with very limited stock… We still remember seeing maybe 1 or 2 houses for sale across entire suburbs during the Melbourne lockdowns.

Some of the Auctions we attended were hard to believe…

How unique was 2021? Can you give us any example that epitomised what was going on?

Gina’s answer:

In February 2022, we saw peak mania from buyers.

Houses were selling within days with multiple offers no matter the location or condition of the property.

As an agent, the signs were evident that this was going to end badly when I couldn’t pinpoint market/offer values.

The extremely low inventory levels coupled with prices rising almost on a weekly basis was creating extreme fear of missing out (FOMO).

When was the first rate hike in Canada, and when did the market slow down?

Gina’s answer:

The slowdown here in Canada was immediate.

The Bank of Canada (Canadian central bank) raised the cash rate for the first time in March 2022

The average home price across Canada dipped immediately and continued falling as rates continued to rise.

How did the market respond to consecutive rate rises, and what is the current sentiment in the market?

Gina’s answer:

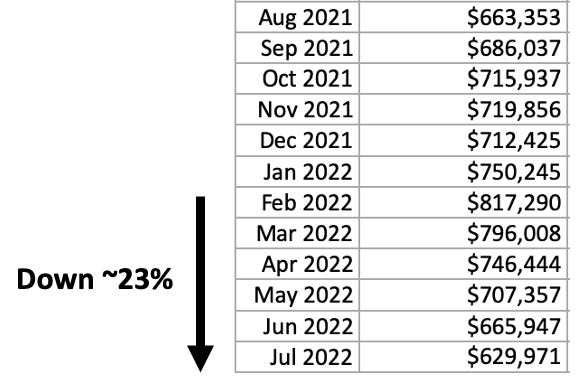

The average price across Canada went from $817,290 in Feb-2022 to $629,971 in July 2022.

See the list below from the Canadian Real Estate Association.

Markets that had gone up the most during the 2020-2021 mania have been impacted the most so far.

Some parts of Toronto have already seen a decline in prices on a year-on-year basis for certain property types.

Buyer sentiment has changed significantly, buyers are still buying, but volume is down from last year across Canada.

“Months of inventory” have gone from 1.7 to 3.4 (which is still low compared to historical averages).

Buyers are waiting for the next hikes to see where the market goes.

Our take:

This, again, sounds similar to what we are experiencing across Sydney/Melbourne.

Real estate agents are calling for a bottom, and most of the property influencers all over social media are saying “the time to buy is now” before (in their words) “the market does what it always does and goes up again”.

The sentiment is almost mirrored, where most people are looking to add to their “investment” portfolios.

How would you compare 2022 to last year, and have you ever experienced anything like this before?

Gina’s answer:

2022 is unlike any other downturn I’ve experienced as an agent.

I was licensed in 2005, the Global Financial Crisis (GFC) 2008 was not a big deal in Canada, and 2017 was different because high inflation was not at play at the time.

Our take:

Another area of similarities between Canada and Australia.

We also managed to dodge the GFC of 2008 relatively unscathed.

How are vendors reacting to increases in interest rates and the subsequent decreases in prices?

Gina’s answer:

Vendors that have to sell have taken a hit.

A lot of buyers who were swept up in the mania of 2021 and part of 2022 were first home buyers and are now experiencing “buyers regret”.

I am also seeing appraisal gaps across the board, with buyers not being able to borrow the amount of money they need to be able to close a purchase.

I am also seeing properties that were taken off the market (with the hope of prices rebounding) getting relisted and sold for far less than what they were fetching at the height of the market.

Additionally, I’m seeing sellers that are unable to sell hold on to properties and rent them out instead of selling at current market value.

As is the case, though, buyers are always faster to catch up to down trends than sellers.

Our take:

This sounds awfully familiar…

Just last week, Tom Panos came out saying, “people not needing to sell would be the reason why property prices wouldn’t fall.

We think this will change very quickly as most households realise they need to service a mortgage almost 3x higher than when they first purchased their homes.

We think “need to sell” will become a reality for many people going into the end of this year.

How about the developers/builders - how are they reacting to the changes in market sentiment?

Gina’s answer:

Some developers have cancelled projects.

For the projects launched during the peak mania in February, the developers are offering crazy amounts of incentives to encourage buyers.

Many buyers are unwilling to lock in a price in a falling market which is impacting pre-sales.

The assignment (nomination sale here in Australia) market is an interesting space. People unable to close on these pre-sale purchases are trying to offload before settlement.

The area being hit the hardest is the pre-construction area.

Our take:

The pre-construction area is also suffering here in Aus, with dwelling approvals in July down 17.2%.

What is interesting from Gina’s response is the impact on the nomination sale market and the issues experienced by buyers who had purchased pre-sales during the market's peak.

The same is happening across the outer suburbs of Sydney and Melbourne, where buyers purchased land subdivisions at peak prices but are now having them revalued significantly lower by the banks comes time to settle.

We think this is an area where there will be significant stress over the coming months.

Anecdotally we know of multiple people who purchased several lots with no intention ever to settle, speculating on price increases and a FOMO-filled nomination sale market where they could sell their contracts for a premium.

We think, just like in Canada, this area will be hit extremely hard.

Any closing remarks?

Gina’s answer:

Long-term Canadian Real Estate fundamentals exist that will not allow for a total collapse.

Short term, we have experienced pain and will likely experience more pain until there’s a shift in monetary policy from the Bank of Canada.

One thing that hasn't changed is “affordability”.

When we compare repayments now vs repayments at the height, the numbers are comparable.

This basically means prices have adjusted so that repayments have stayed at similar levels based on different interest rates.

I’m personally a firm believer that lower property prices and higher rates are more favourable to buyers in the long term.

Our take:

We agree with Gina here that lower property prices with higher interest rates encourage a more vibrant economy where capital is being poured into PRODUCTIVE investment instead of being pushed into speculating on property price growth.

The only difference is that, unlike in Vancouver and Toronto, where prices have adjusted to the increase in cash rates by falling up to 26%, the same can't be said of Sydney and Melbourne.

We think Sydney and Melbourne aren’t immune to the wrecking ball that is rising cash rates and expect the carnage that is sweeping Canada to become a reality across both these major cities over the coming months.

Watch this space.

Property dashboard:

For those who are reading this blog for the first time, we just released a property dashboard where we put together a wrap-up of everything property across the NSW/VIC markets.

In our dashboard, you can find the following:

Our property data wrap for the week.

The feature article for the week

The chart of the week

Subscribe to get the email in your inbox every Tuesday/Wednesday evening.