Builders going bust

Builders going bust

How should I be feeling about this?

A profitless boom? What does that even mean?

What’s on our mind: We have heard the term “profitless boom” get thrown around by builders, but what the hell does that even mean, and why does it matter?

What happened this week: Westpac consumer sentiment down 3%, US inflation rate comes in under forecast at 8.5%.

What are we watching next week: RBA minutes, Australia unemployment rate, New Zealand cash rate decision

Prelude:

This isn’t a meme… seriously

What’s on our mind:

The origins of the construction industry’s problems began in 2021.

Housing prices were soaring by more than 25% annually across Sydney and Melbourne, and the resultant price signals sent the development market into a frenzy.

It is no surprise that increasing home prices give the market more of an impetus to accelerate the development of new projects, which can then be sold at high prices.

The profit becomes irresistible.

To illustrate this point, here is a hypothetical scenario:

You own an empty block of land in the outer suburbs of Sydney worth $500,000.

Your neighbour sells their newly built home on an identical block for $1,250,000.

The cost to build something identical to theirs is $500,000.

You now have a potential profit of $250,000.

This gives the landowner 250,000 reasons to immediately sign a contract with a builder to get that home built and on the market as soon as possible.

In economics, this is called a “price signal” - all it does is tell consumers and producers (via prices paid) whether or not supply should be increased or decreased.

If prices are rising, the respective industry will respond by building more homes (increasing supply) to bring prices back into equilibrium or, at the very least, alleviate upwards pressures.

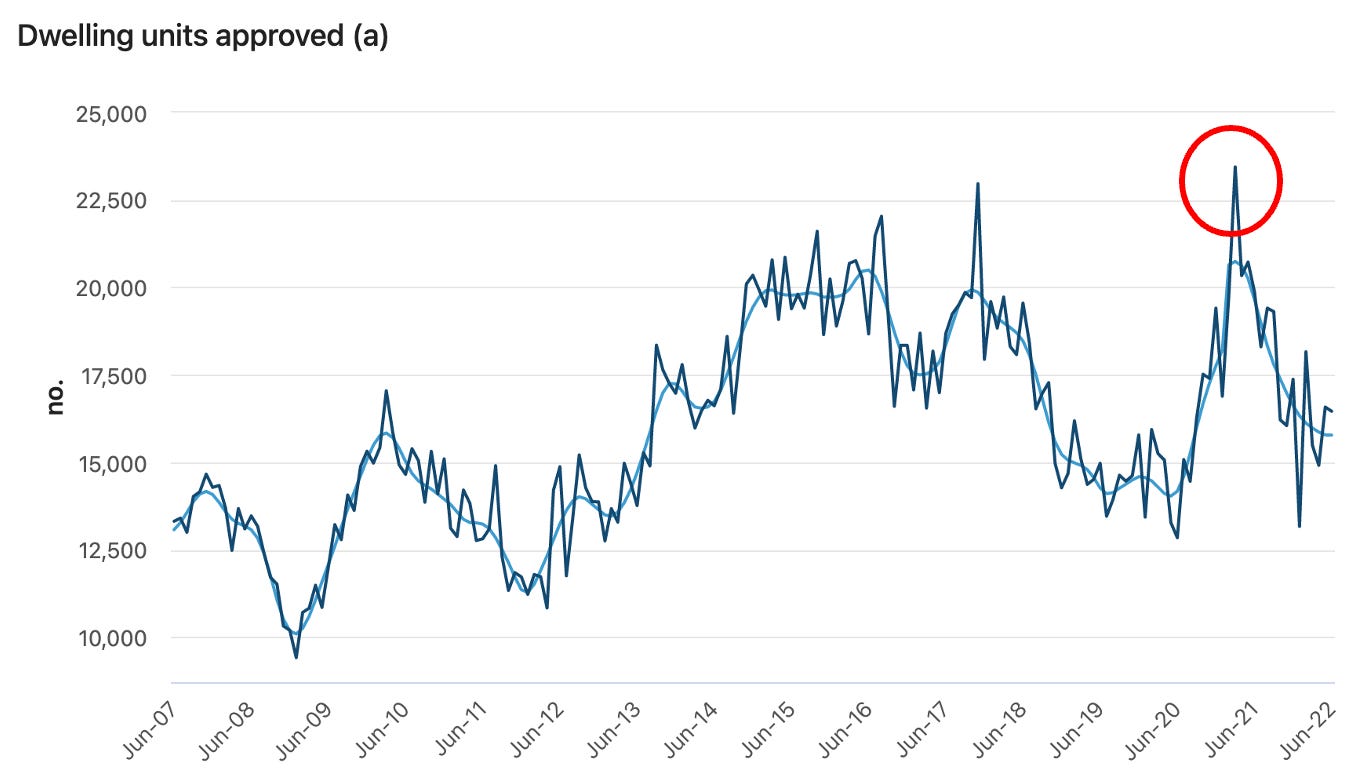

The price signals were so strong in 2021 that dwelling approvals briefly touched almost 15-year highs.

These approvals naturally lead to increased demand for building works.

All of this demand led to an increase in overall construction activity, something you would expect the industry would celebrate as the “good times”.

But less than 12 months later, why are builders going bust?

Why is HIA (housing industry association) chief economist Tim Reardon saying a “Profitless boom is an accurate turn of phrase”?

Why is the NSW building commissioner David Chandler's resigning?

This week we detail what we think is happening across the industry and what we think this means for house prices.

The average property spruiker will tell you a fall in construction activity can only be good for housing prices because it means less supply.

We think the opposite is the case… read on to see why.

Building companies going bust - why it matters.

After days of debating this internally, we think the best way to think about this is in four parts:

Increasing interest rates decrease demand for NEW construction - Everything starts with the cost of debt. The higher the cash rate goes, the less compelling new builds become.

Why builders are going bust NOW - Increasing labour and materials costs versus fixed price contracts signed in 2020-2021 creating losses.

What does it mean when a builder “goes bust”? - Employees without a job, subcontractors unpaid and customers with unfinished homes. The worst part is that none of the debts incurred disappear.

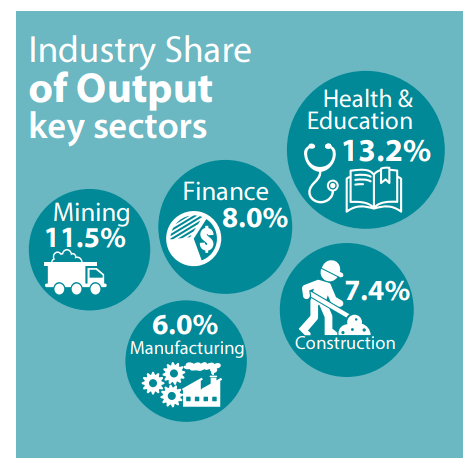

Why all of this matters - The building and construction industry makes up ~7.4% of the Australian economy and makes up (directly) ~9% of the Australian workforce.

1) Interest rates rising decrease demand for NEW construction

Interest rates matter a lot, and believe it or not, it impacts the demand for NEW construction activity.

The key here is to understand HOW higher rates impact consumer demand for new homes and how that flows through to the construction industry.

For example, the average person is trying to decide between renting a property or building their first home.

If that person needs to borrow $600,000 to purchase and build on a new block of land, the decision to build a new home makes a lot of sense when the interest rate is 2%. The interest payments on that loan would be $12,000 per annum ($1,000 per month).

Less than someone would need to pay for a rental property in Sydney and Melbourne.

Now take that same situation and apply a 4% interest rate. That same loan now costs $24,000 per annum ($2,000 per month).

Suddenly, the consumer might think twice about signing a contract with a builder.

The impact on the industry is LESS work for builders as rates rise.

2) Why are builders going bust now and not 12 months later when there is less work?

This is because builders took on fixed-price build contracts in 2020 and 2021.

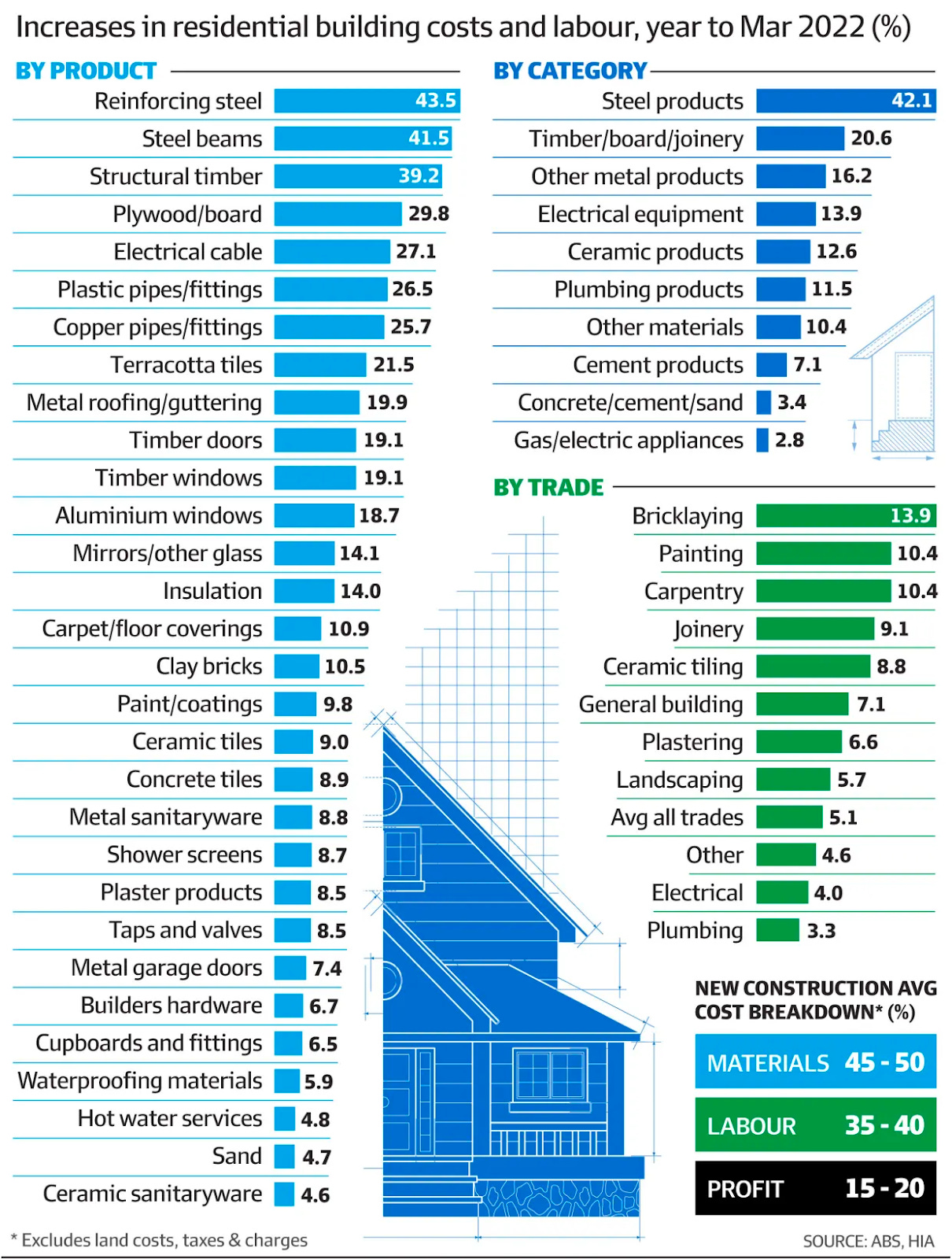

Since then, the costs of materials have increased from anywhere between 4% to as high as 43.5%, some examples being:

Reinforcing steel: UP by 43.5%

Structural timber: UP by 39.2%

Electrical cables: UP by 27.1%

To make matters worse, the labour rates being paid to the subcontractors have also increased, with some notable increases coming from:

Bricklayers: UP 13.9%

Painting: UP 10.4%

Carpenters: 10.4%

The image below paints a more wholistic view of prices through to March 2022:

The part that interests us is the 15-20% profit margin the builder typically builds into a contract price.

With the cost of materials and labour increasing and time delays caused by supply chain issues, builders quickly see their margins evaporate.

A hypothetical run-through of this to help visualise it:

A builder signed a contract to build a home for $500,000 with a 20% margin on the total contract sum.

Before the materials/labour price hikes, the builder would make $100,000 (before paying any taxes).

Material prices are now up 15% and labour another 15%; the project cost has now gone from $400,000 to $475,000.

The builder is left with a potential $25,000 profit on the job, assuming they can finish it in the scheduled time.

Factor in the supply chain issues and the builder is out by two months on the scheduled completion time for the project, all whilst paying staff, rent and whatever interest on any project that needs to be funded before bank drawdowns can happen.

That potential $25,000 profit that may or may not has been left is now well and truly gone, and the job becomes loss-making for the builder.

Because of these dynamics, any contract signed in 2019-2020-2021 is what we would consider “at-risk contracts”.

The only way these builders can fill in the gaps from these contracts is by signing NEW contracts where they can turn a profit and make up for previous losses.

Otherwise, they risk insolvency.

Speaking of… we have a feeling insolvency rules aren’t very well understood, and so many of these guys are racking up debts with suppliers and hoping they can turn around their fortunes.

For those who are interested, they can read the following: Determining insolvency in the construction industry.

3) What does “going bust” mean, and what is left when a builder walks off-site?

The simple answer is unpaid employees, unpaid subcontractors, unfinished homes and a pile of debt attached to all of it.

The unpaid employees all likely have mortgages that they may struggle to repay.

The unpaid contractors are now out of pocket for all of the money the builder owes them.

The worst part is that the unfinished homes are left in the hands of those who can least afford them.

These people would have invested all their hard-earned savings into their homes and taken out a loan to finance the remainder of the build.

In the end, the builder goes into administration, the subcontractor’s risk going insolvent, the employees become unemployed, and the homeowners are left with unfinished houses with no way of completing the build.

A situation where no one is a winner.

4) So why does all of this matter?

Property spruikers understandably are looking for optimistic takes front this mess, and we have seen some calling for this being good for property prices.

The thinking seems to be that the value of existing properties will be higher with less new supply coming onto the market.

The reality is no good comes from this situation.

Building and construction comprise ~7.4% of the Australian economy (as of 3 August 2022).

Across NSW and VIC, the building and construction industries contribute to between 5-12% of either state’s economy.

In terms of employment, the share is even more significant, with ~9% of all Australians directly employed in the industry.

Construction activity, therefore, impacts employment. As employment starts to decrease, the buying power of the consumer decreases.

With less employment, naturally, there is less demand for new home builds, leading to less work for builders and more builders going bust.

Like an avalanche, the situation builds momentum and worsens as the loop repeats.

The only thing holding up the bullish thesis for property prices is Australia’s record low unemployment rate of 3.5%.

If we start to see the unemployment rate tick up, we see no foundation left to prop up the bullish thesis.

This is why we think no good comes from bankruptcies in the construction industry and why we are watching the space very closely.

Media review:

TLDR summary:

Melbourne-based builder (Blint Builders) goes bust, owing $1M to over 50 creditors.

Liquidators commented on “half a dozen” that were impacted by Blint’s demise, many of whom are unsure how they will pay for the leftover construction costs.

Our take:

A clear example of nothing good coming from these insolvencies.

The builder goes bust, but none of the debts goes away.

The employees lose their incomes, the subcontractors are out of pocket >$1M creditors, and the homeowners are left with unfinished homes and no way to pay for the remaining costs, having already handed over all their saved-up capital.

The ripple effect compounds into as worse an outcome as possible.

TLDR summary:

Hotondo Homes Hobart goes bust with 80 subcontractors and 40 homeowners in limbo.

One Tasmanian couple is out of pocket $260,000 for a wall and partially built garage.

Some tradies owed between $75,000 and $100,000 from work already completed.

Our take:

This one needs no explanation.

A builder going bust leaves 80 subcontractors with receivables that are now never likely to be paid and 40 homeowners with unfinished homes.

No positives to take away from this story either.

TLDR summary:

Western Sydney high-rise apartment developer Merhis Group

Five other Merhis Group companies had already been liquidated, potentially owing $17m.

The liquidators’ investigations into the Stacey Group’s financial affairs identified potential voidable transactions and insolvent trading claims >$25 million.

Our take:

This one is a little different…

It involves the collapse of a development company and its subsidiaries with over $17m in debts at the time of being put into administration.

These developers are in charge of bringing new supplies onto the market.

These guys are at the top of the food chain in the construction industry - the guys in charge of the money.

If there are stresses at the financial allocator level, then the rest of the industry will likely suffer something serious.

The Merhi saga is a mix of unpaid debts and alleged poor quality control concerning construction practices.

Property dashboard:

For those who are reading this blog for the first time, we just released a property dashboard where we put together a wrap-up of everything property across the NSW/VIC markets.

In our dashboard, you can find the following:

Our property data wrap for the week.

The feature article for the week.

The chart of the week.

Hi team, I saw no comments posted so I thought I’d at least say thanks for taking the time to publish what you do - and you translate it into English so Joe 6-pack can easily understand. Not a first time reader, but credit where credit is due. Thank you for doing what you do