How bond markets impact property prices

How bond markets impact property prices

What are bonds and why do they matter?

What do bond yields mean for the property market?

What’s on our mind: Bond yields are exploding higher. What is a bond and why should a property investor/owner care?

What happened this week: US Fed increased its cash rate to 1.75% (up by 0.75%).

What are we watching next week: RBA June meeting minutes, UK/Canada/Japan CPI (inflation rate)

Prelude:

What’s on our mind:

What the heck is a bond and why should we care?

The flavour of the week in mainstream media was BONDS. All week the talk was about bond yields rising and how the share market was in free fall reacting to this news.

We then got the US federal reserve to come out and hike its cash rate to 1.75% (up by 0.75%) and the UK follow suit a few days later increasing its cash rate to 1.25% (up by 0.25%).

This led to bond yields rising even more and the share market selling off in tandem.

This is a property-focused newsletter so the question we want to answer today is - What do rising bond yields mean for the property markets?

Over the last 30 years through periods of high inflation, low inflation, high bond yields, and low bond yields, property prices continued rising. So you could be forgiven for thinking the property market is immune to all of this (It would be un-Australian to think otherwise anyway).

This time we think it's important to pay attention to the things happening in the “bond markets”.

First of all, what are bonds, and what are yields?

Bonds are simply banking jargon for what we the common folk know as loans.

They are simply a transaction between a borrower and a lender, an example would be a $1,000,000 loan made with a fixed 5% interest rate.

The yield component is a reference to the interest being received for making that loan. For the same loan, we mentioned above the “Bond yield” would be 5%.

The market for bonds is massive and if we decided to spend the rest of this write-up going down the rabbit hole of what they mean for the broader economy, we would have no time left to talk about the property markets.

In the interest of staying awake at a very high level the key takeaway, we will focus on is the fact that the bond market determines the PRICE OF MONEY (The interest rate a borrower pays to a lender to get their hands on cash).

This means that they give a signal to folks where the natural cost of borrowing sits in the free market on any given loan with any given fixed-term maturity.

As an example, if the yield on a 5-year bond is trading at 4.5%, this means investors expect to be paid an interest rate of 4.5% on a 5-year fixed-rate loan.

Now that we have determined what a bond is and what the yield is referencing it’s also important to know which type of bond the mainstream media likes to focus on.

So which bonds does the media focus on?

When quoting “bond yields” the media almost always refer to government bonds.

They will say, "the yield on a 10-year government bond is now trading at 5%”.

This means that if the government were to try and take out a 10-year fixed-rate loan they would need to pay an interest rate of 5% per annum.

Why is this important? - Because these are loans being written to the Australian government, the most credit-worthy borrower in Australia (or at least you would hope this is the case).

Being the most credit-worthy borrower comes with the privilege of being able to get the BEST interest rates on offer.

This is why bond yields DO NOT equal mortgage rates, but that doesn't mean they are not related.

In summary, bond yields = the interest rate that needs to be paid to borrow money.

If the government is having to pay a certain interest rate to borrow, then it will eventually translate to a higher borrowing rate for the average mortgage holder.

After all, why would a bank write a loan to an average Australian at a lower interest rate when it could lend to the Australian government at a much higher rate.

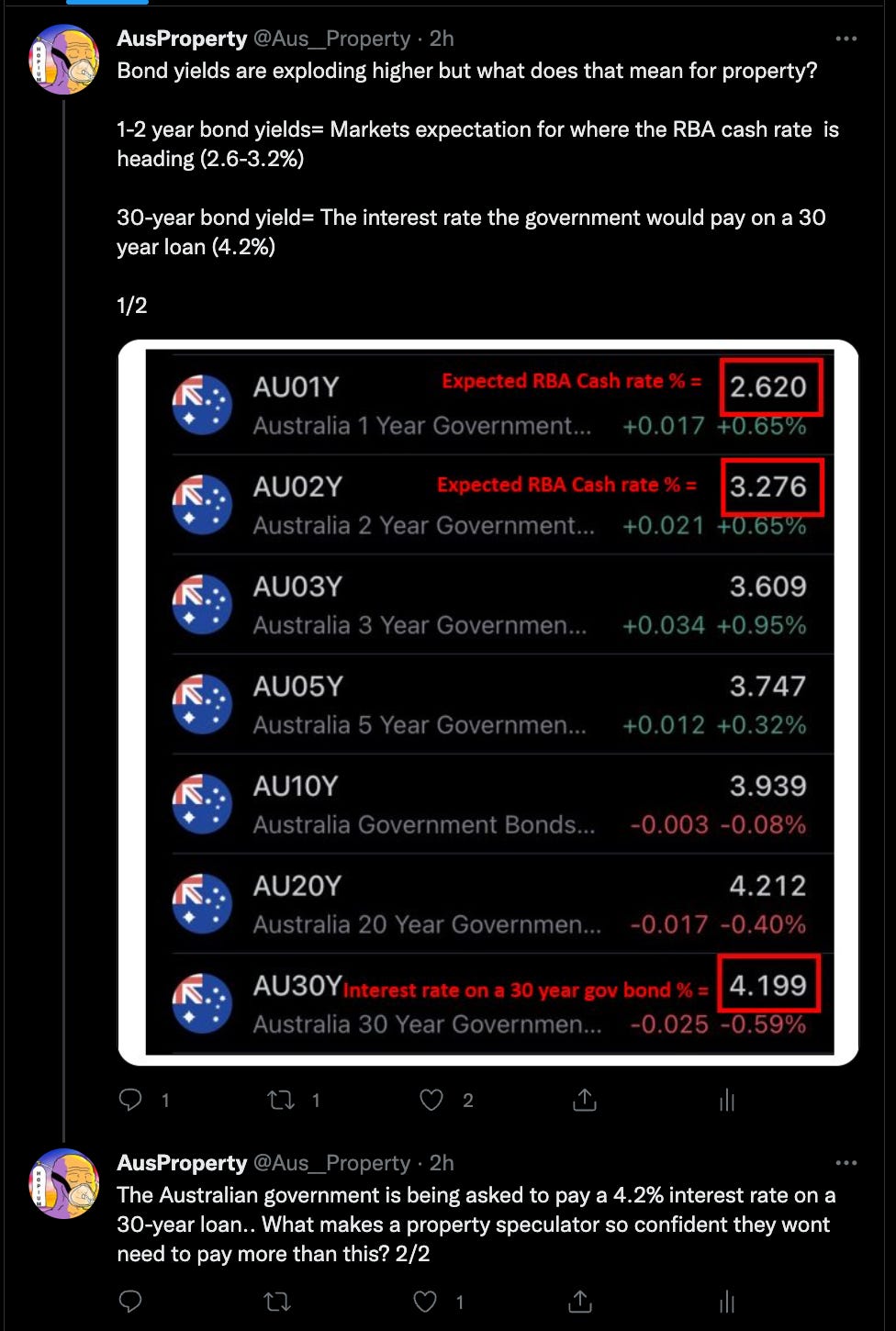

We covered this connection in a tweet we did earlier in the week which you can view below.

Subscribe to our Twitter account to see our ramblings daily.

What did the bond markets do this week?

So we now know what a bond yield is and how it impacts borrowing costs.

We know that bonds set the PRICE OF MONEY (the interest rate needed to be paid to get a loan).

We know that the yield on a 30-year government bond yield is a signal for where mortgage rates are headed (hint - they go higher).

Government bond yields matter because they are the rates being offered to the most credit-worthy borrower in Australia - the Australian government. (Another hint - We should expect to pay a lot more than they pay).

So how did the bond market do this week and what is it telling us?

This is telling us that the Aus government would need to pay a fixed interest rate of 4.1% if it were to borrow money for 10 years.

Usually, this is a precursor for the RBA cash rate.

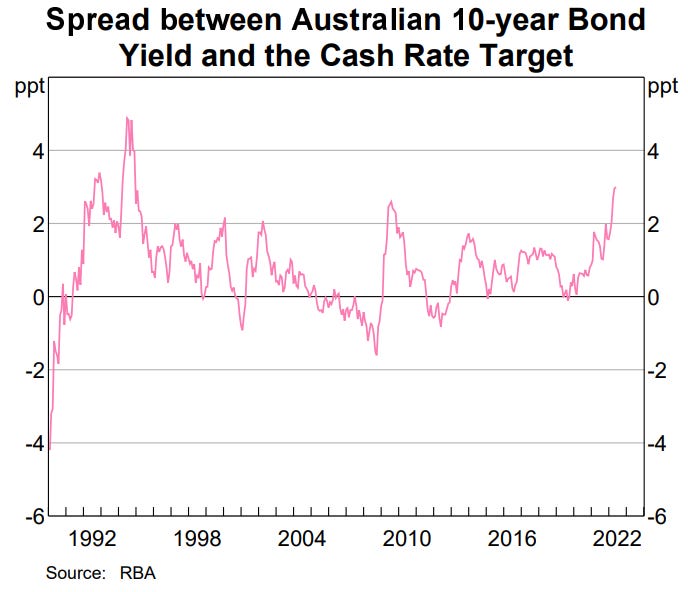

The chart below shows the long-term correlation between the 10-year bond yield and the RBA cash rate target. Since the early 1990’s the difference between the two has been between 0 and 2%.

With the 10-year yield currently trading at 4.1%, using the 0-2% as a guide, the RBA cash rate is likely to converge to sit somewhere between 2.1 and 4.1%.

The next question is if the RBA cash rate is headed to 2.1-4.1%, where are mortgage rates headed?

Below are two charts that give us an approximate estimate.

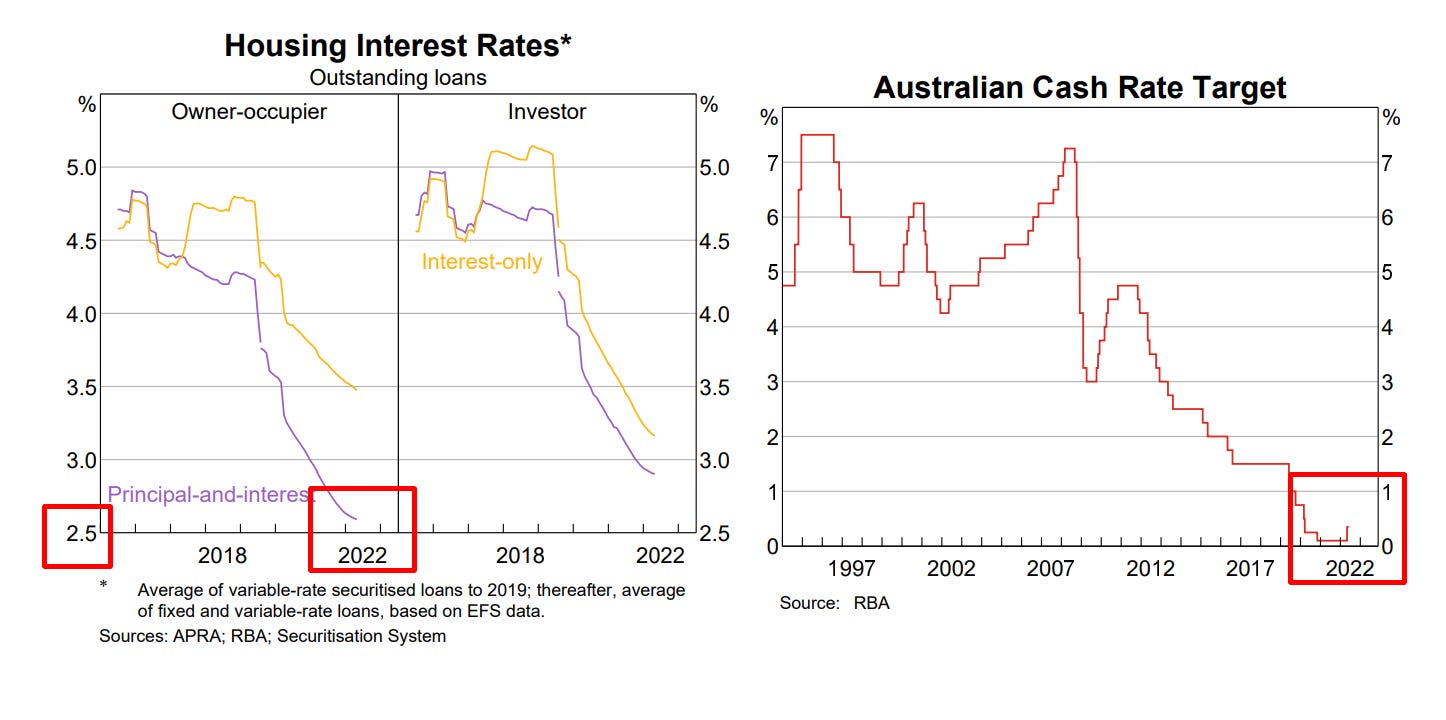

When the cash rate was sitting at 0.1% for most of 2020-2021, the lowest mortgage rates being offered by the banks were around the ~2-2.5% range - This gives a ~2% difference between the cash rate and mortgage rates.

If we then take the future expected cash rate that we worked out above and apply a 2% premium to it, the number we get for where Australian mortgage rates are headed is somewhere between 4.5 to 6.5%.

So the last time we saw a 2-4% RBA cash rate, variable interest rates on a mortgage were at 4.5-6.5%.

What about all the other bond yields?

We focused mostly on short-dated bonds for today’s article because mortgage rates are mostly financed based on these rates, this doesn't mean the longer-dated (30-year) yields don't matter though.

After all, almost every housing loan written in Australia is written based on a 30-year payback period.

This week, the 30-year government bond yield hit a high of 4.3%. This means that the Australian government would have to pay an interest rate of 4.3% to take out a 30-year loan.

For some comparison, mortgage rates in Australia are currently being written for as low as ~2.8-9%.

This sort of market structure where John Citizen can borrow from a bank at a lower interest rate versus the Australian government is perplexing.

Do the big banks think that the Australian government is a riskier borrower than a real estate agent or a first home buyer working odd jobs to pay off their mortgage?

Or is this just a short-term mispricing that will even out over the coming months?

Our view is that mortgage rates will need to catch up to and may even surpass the yields (interest rates) that these government bonds are pricing.

There are only two scenarios for how this plays out, either:

Government bond yields start to fall and mortgage rates stay the same.

ORMortgage rates increase, catching up to and possibly surpassing these bond yields.

It will be interesting to see what the RBA does at the July meeting, but the likelihood of scenario B playing out is where we have placed our bets.

After all the RBA cash rate will largely determine the direction in which mortgage rates move in the short term.

Why do bond yields matter and what do they mean for the property market?

Bringing all of this information together.

One way to think about the lending dilemma is to put yourself in the shoes of a LENDER, would you rather lend to the average person off the street to buy a house at a 4% interest rate, or would you rather lend to the federal government at the same rate.

The answer to this question is obvious, the federal government is much less likely to go bankrupt, and is a whole lot likelier to pay its interest repayments on time so you would write the loan to the government.

Would you be tempted to loan to the average Australian if they were willing to pay you a 2% higher interest rate? Maybe.

This is the same way a bank thinks when making a lending decision, this is why we have seen fixed interest rates for loans move so high so quickly.

Because of this credit growth WILL slow.

The fact is bond yields being where they are will hurt credit growth.

Putting aside the dilemma banks will face when making lending decisions, there will also be fewer borrowers when a mortgage has a 6% interest rate attached to it than if it was being offered with a 2.5% interest rate.

We covered what we think slowing credit growth will mean for property prices in our last article which you can read here: What happened in 2021 stays in 2021

For those of you who have done enough reading for today, if there is one thing you should take away from today's article it is as follows:

Higher bond yields will inevitably lead to higher interest rates on residential mortgages.

Higher mortgage rates will reduce demand for new loans.

When credit growth slows (or worse, goes negative) property prices WILL start to stagnate/fall.

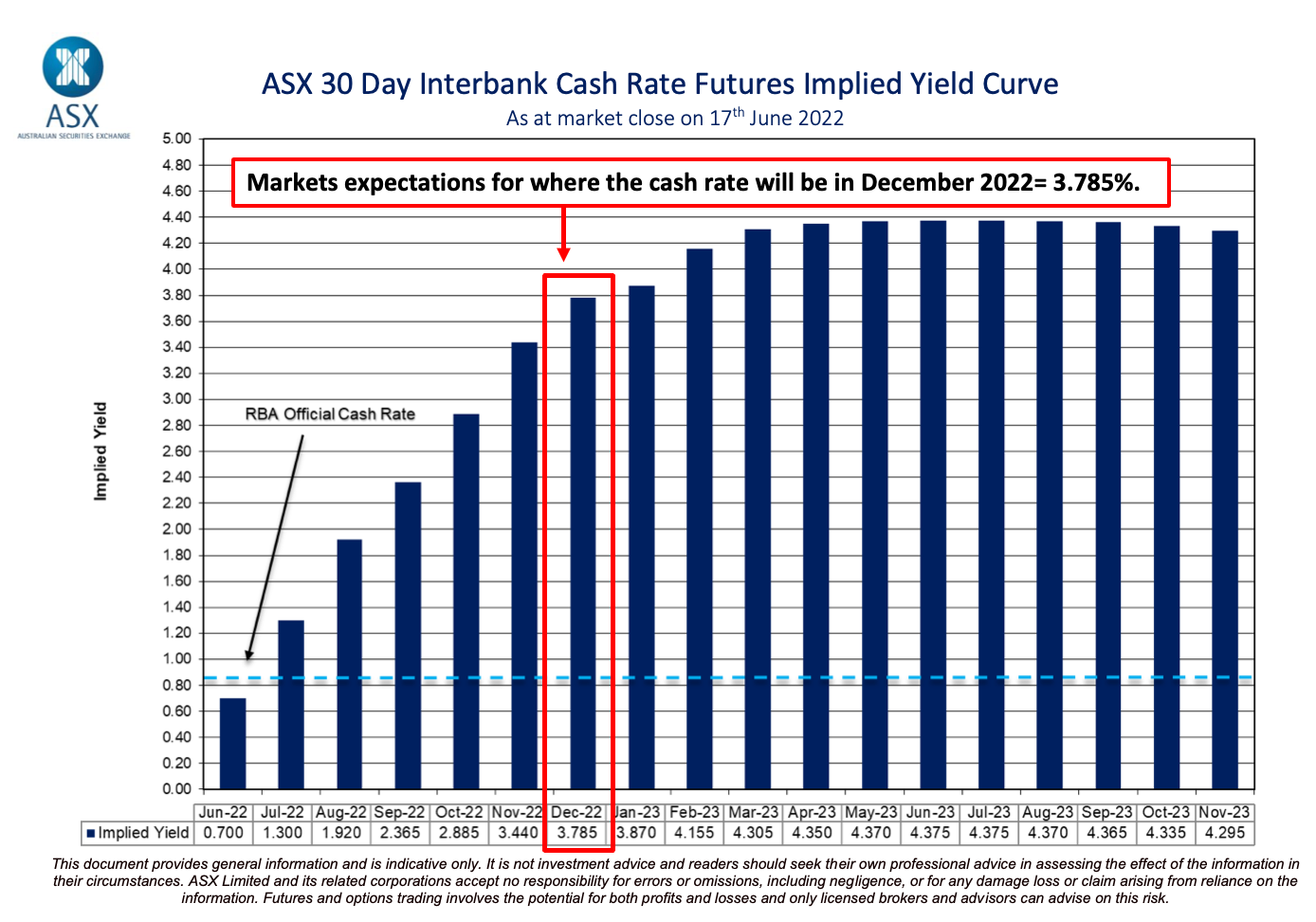

Below is the latest set of market expectations for the RBA cash rate, pricing in a ~3.8% cash rate by December. If the property market is reacting the way it is now to a 0.85% RBA cash rate then we think things will look a lot worse in the second half of this year...