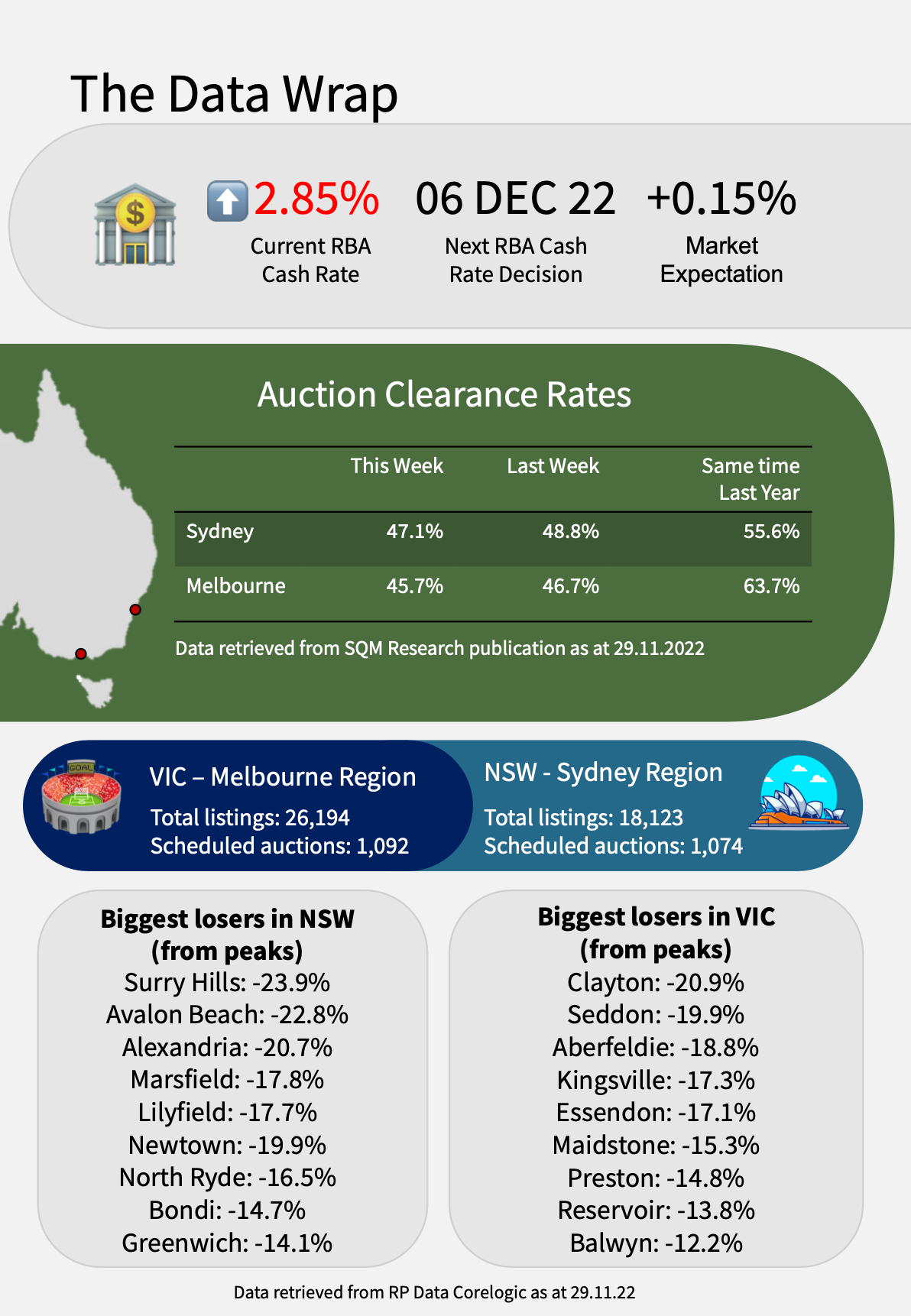

All things property this week

All things property this week

Everything you need to know...

Property Down Under - 30th November 2022

The feature article of the week:

Below is our feature article for this week’s edition of the newsletter.

This is the article we found most interesting to read, and the one we think is a “must read” for all our readers.

Our key takeaways:

Early signs of mortgage stress starting to emerge after seven rate hikes by the RBA.

Tens of thousands of fixed-cost loans expire in the middle and second half of 2023. This is expected to put pressure on the home loan market.

More Australians have sought access to funds via non-traditional pathways. Non-conforming loans almost doubled between 2019 and 2020 to almost $16BN in September 2022.

Home loan settlement platform PEXA is seeing a large number of borrowers in outer suburban areas refinancing. This signals borrowers in those areas are more sensitive to the recent spate of rate rises.

Online lending (TicToc) boss Anthony Baum said many borrowers coming to him trying to refinance were being caught out by the shift in rates.

Our Take:

This article primarily tip toes around the upcoming fixed rate mortgage cliff in 2023.

Between now and the end of 2023 ~$158BN in fixed rate mortgages will be due to expire and require refinancing.

Whilst some of these loans were written using 1.6-2% fixed rates, the market rates for mortgages are now at >5% - almost 3x higher than when the loan was first written.

We touched on all of this in our latest article which you can read here: Higher rates for longer and a looming refinancing crisis.

We think that this will be the trigger for more “forced selling” or at least deleveraging by those who are caught out by the higher than expected rates.

After all this is one of the most aggressive rate hiking cycles done by the RBA in over 20 years.

More importantly though, the higher interest rates will make debt less attractive for investors and home owners alike, this will impact credit growth.

Other Mainstream media 📰

Rate rises take 14pc bite out of East Melbourne office sale (AFR)

Vendors slash house prices by up to $865k as selling gets tougher (AFR)

Housing affordability set to worsen despite falling house prices (AFR)

Chinese offload Aussie apartments as home economic crunch hits: Robert Gottliebsen (The Australian)

Recovery on the way for capital city home prices: SQM Research (The Australian)

Greater choice for buyers but interest rates tighten budgets (The Australian)

Why should you care:

The chart above shows new loan commitments for housing (credit growth).

This is what we believe drives house price growth.

Our takeaway:

Lending data for the month of September:

Total home lending fell 8.2%.

Owner occupier lending fell 7.2%.

Investor lending fell 10.3%.

Our expectation:

Our theory is that for there to be an increase in property prices, credit growth for housing needs to be positive and increasing.

The charts above show that credit growth has started to fall off a cliff.

The last two times this happened was in 2007-2008 in the fall out of the Global Financial Crisis and again in late 2019 due to the royal commission into banking.

We think that wherever these lending indicators trend, house prices will follow. I.e credit growth decreasing will lead to lower prices.

Watch this space.