All Thing's Property This Week

All Thing's Property This Week

Everything you need to know

Property Down Under Newsletter - 14th September 2022

The feature article of the week:

Below is our feature article for this week’s edition of the newsletter.

This is the article we found most interesting to read, and the one we think is a “must read” for all our readers.

Key takeaways:

Borrowing costs globally are squeezing homebuyers and property owners. Canada and Australia are facing price declines in the double digits.

Former Bank of Japan economist Hideaki Hirata says, “We will observe a globally synchronized housing market downturn in 2023 and 2024,”. He also warns the full impact of this year’s aggressive rate hikes will take time to play out for households.

Australia recorded its largest monthly decline in home prices in almost four decades.

In Sweden, formerly one of Europe’s hottest markets, home prices have fallen about 8% since the spring, with most economists expecting a 15% drop.

HSBC Holdings Plc has warned the UK is on the “cusp of a housing downturn”.

Our Take:

The major takeaway from this article is that a property downturn cannot be viewed with a purely domestic lens.

Global markets and financial systems are so intertwined these days that changes in economic conditions in other parts of the world have a trickle-down impact on what happens to home prices domestically.

Right now, the entire world is experiencing high inflationary pressures, forcing central banks (worldwide) to jack up interest rates.

Unsurprisingly, the increase in borrowing costs is impacting asset prices worldwide.

With the US coming out with higher-than-expected inflation numbers overnight, we think this will be a continuing theme over the next 6-9 months and expect to see increasing interest rates.

The simple high-level summary of this article and the situation we find ourselves in is:

High inflation leads to higher interest rates.

Higher interest rates mean debt becomes more expensive to service.

Higher servicing costs lead to lower borrowing power.

Lower borrowing power leads to lower asset prices.

Property prices across Sydney and Melbourne will not be immune to this^.

Other Mainstream media 📰

National residential vacancy rate falls to 16-year low (AFR)

‘Hard pill’ to swallow: terrace owner cuts price hopes by $250,000 (AFR)

Grim prediction Australia facing major housing crash (News.com.au)

The neighbourhoods where property prices are still higher than a year ago (Domain)

Era of through-the-roof house prices in Australia set to end (Reuters)

Why should you care:

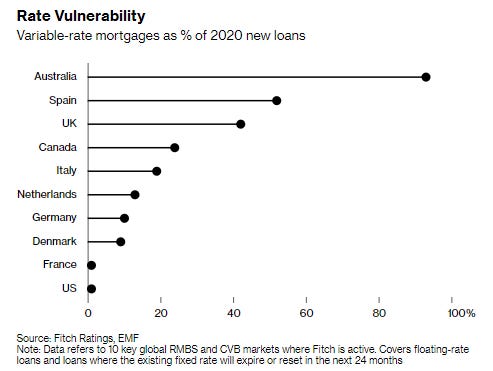

How exposed borrowers are to rising rates varies, some countries write a higher % of variable rate mortgages whilst others opt for fixed-rate mortgages.

According to a May report from Fitch Ratings, Australia, Spain, the UK, and Canada had the highest variable-rate loans as a share of new originations in 2020.

New Zealand has ~55% of the outstanding value of residential mortgages, either floating or fixed rates, that need to be renewed in the year to July 2023.

Our takeaway:

In 2020 over 90% of loans written were all variable rate mortgages, the highest of any developed economy and almost double Spain, which comes in second.

This means that the Australian borrowers who took out mortgages over the last two years are most susceptible to increases in interest rates.

Our expectation:

We think that as the RBA is forced to raise rates, the pressure on households predominantly on variable-rate mortgages will become unbearable.

With most of the fixed rate mortgages set for expiry late this year and throughout 2023, we also expect to see a large cohort of borrowers realise that they cannot service a mortgage with an interest rate double where it was when they first purchased a property.

We think this will lead to more forced selling and lower property prices over the coming 6-9 months.

Thanks for the update.

Rarely mentioned is that investors will soon have access to 3-4% cash rates, one of the reasons they moved to property/shares. Plus leverage at very low rates.

Interest free risk to risk free interest.